How a Nigerian Salary Earner Actually Starts Building Assets

In Nigeria, one of the most persistent financial misunderstandings is the belief that a higher salary automatically leads to wealth. It does not. Many workers increase their income over time yet remain permanently financially fragile. A civil servant earning ₦180,000 per month and a trader making ₦600,000 per month may appear to live in different economic worlds, but both can retire with nothing if they never convert income into assets.

The core issue is simple: most people confuse cash flow with wealth.

Economists and financial thinkers have warned about this for decades. The American economist Robert Kiyosaki famously distinguished between income and assets by defining an asset as something that “puts money in your pocket whether you work or not.” Warren Buffett expresses the same idea more formally: wealth is the ability to sustain your standard of living without active labour. The implication is direct — salary alone cannot guarantee long-term financial security because salary depends on continued employment. Assets, however, generate income independent of your daily effort.

This article explains how a Nigerian salary earner begins the transition from working for money to having money work for them.

The Three Financial States

Before building assets, a worker must understand where they currently stand financially. Most Nigerians unknowingly remain trapped in the first stage throughout their working life.

1. Survival

In the survival stage, salary exists only to pay immediate bills:

- rent

- transportation

- feeding

- utilities

- family obligations

At this level, the month ends when the money ends. There is no buffer. An unexpected hospital bill, job loss, or salary delay immediately creates crisis. Many workers in both public and private sectors are here regardless of their job title.

2. Stability

Stability begins when the salary is no longer fully consumed by expenses. The worker now has:

- small savings

- an emergency reserve

- some financial breathing space

This is a critical turning point. According to behavioural economists like Richard Thaler, financial security begins not when income increases, but when decision-making improves. The presence of a buffer changes how a person thinks. They no longer make purely reactive financial decisions.

3. Wealth

Wealth begins only when income no longer depends entirely on employment. At this stage, assets produce recurring earnings. Even if the person stops working temporarily, money still enters.

This distinction leads to the most important principle of personal finance:

Salary is cash flow.

Assets are financial independence.

A salary feeds you. An asset sustains you.

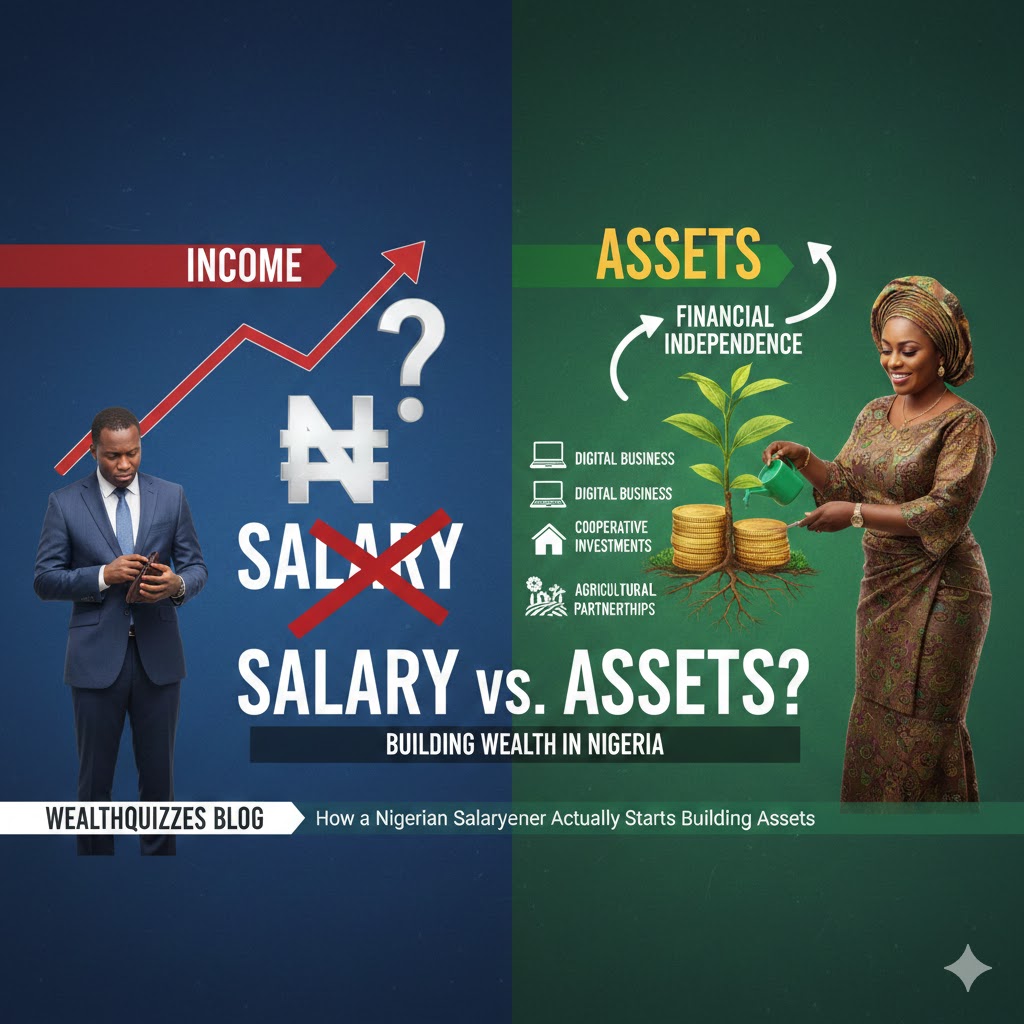

What Actually Counts as an Asset in Nigeria

The idea of assets is often misunderstood locally. Many people assume the first asset must be land or a house. In reality, asset-building follows stages. Early assets are usually income-producing capabilities, not expensive properties.

Below are realistic Nigerian assets a salary earner can begin developing.

1. A Marketable Skill

The first and most accessible asset is a monetizable skill. Examples include:

- legal drafting

- graphic design

- coding

- video editing

- bookkeeping

- tutoring

A skill becomes an asset when it can generate independent income outside your employer. Economists refer to this as human capital. Nobel Prize–winning economist Gary Becker demonstrated that investing in skills increases lifetime earnings more reliably than speculation.

A worker with a skill has two incomes: salary and side earnings. This is the true beginning of asset building.

2. A Profitable Small Digital Business

Digital commerce has lowered entry barriers in Nigeria. A modest online service — document preparation, social media management, educational content, or digital products — can produce recurring revenue. The important factor is repeatability: income should not require restarting from zero each month.

3. Dividend Stocks

Nigeria’s capital market, regulated by the Securities and Exchange Commission (SEC), allows ownership in companies that distribute annual dividends. Though not risk-free, carefully selected dividend-paying stocks can gradually produce passive income. This introduces the salary earner to ownership rather than mere labour.

4. Cooperative Investment Pools

Traditional contribution schemes (esusu, ajo, cooperative societies) can become productive assets when funds are directed into income-generating ventures rather than consumption. Properly structured cooperatives allow members to participate in larger investments otherwise inaccessible individually.

5. Agricultural Partnerships

Nigeria’s agricultural sector offers partnership models where individuals fund production and share profits. When properly vetted, this creates exposure to real-sector productivity rather than speculative trading.

6. Rental Property (Later Stage)

Real estate is often considered the “ultimate asset,” but it should come later. Property becomes viable only after a worker has achieved stability and accumulated capital. Entering real estate too early typically results in debt pressure rather than wealth.

What Is NOT an Asset

One of the most damaging financial habits is mislabeling consumption as investment. Many items that appear impressive actually drain financial capacity.

Financed Cars

A car used primarily for personal transport consumes fuel, maintenance, insurance, and depreciation. It is a convenience, not an asset, unless it directly produces income (e.g., logistics service).

Expensive Rent for Status

Renting beyond one’s affordability bracket is a social decision, not a financial one. It converts future income into present consumption.

Clothing Purchased to Impress

Fashion has social value but zero financial yield. It neither appreciates nor produces cash flow.

Impulse Gadgets

Phones and electronics rapidly depreciate. Buying them frequently is equivalent to repeatedly discarding capital.

Financial historian Thomas Stanley, in The Millionaire Next Door, observed that many high earners remain poor because they “purchase symbols of wealth instead of building wealth itself.” The Nigerian context reflects this perfectly.

The Real Mindset Shift

Most workers ask:

“How can I increase my salary?”

This question keeps a person dependent on employers, promotions, and external decisions. Promotions are uncertain; employers change; industries decline.

The more powerful question is:

“What can start paying me apart from my employer?”

That single shift marks the transition from employee thinking to owner thinking.

When a salary earner begins developing an income-producing skill, saving a buffer, and gradually acquiring small income-generating assets, the future changes fundamentally. Job loss becomes a setback rather than a catastrophe. Retirement becomes optional rather than frightening.

Final Thought

Wealth is not created in a single dramatic moment. It is built quietly through a sequence of decisions: learning, saving, acquiring skills, and owning productive assets. In a volatile economy like Nigeria’s, the greatest financial risk is dependence on one income source.

Income sustains your present life.

Assets protect your future life.

The journey to financial security does not begin when your salary increases. It begins the day your income stops depending on one employer alone.