How Money Is Created: Banking, Credit, and the Illusion of Scarcity

Understanding why modern money is created through credit — not printing — and why access to credit, not cash, determines economic power

Money is not merely the physical cash in your wallet or the coins in your pocket. In modern economies, the vast majority of money exists as bank credit — electronic entries in accounts created every time a loan is made. This reality is poorly understood by many, yet it is one of the most consequential aspects of how modern economies function.

To understand why, we must explore how money is created, who controls this process, and why access to credit — not physical currency — is the real source of economic power.

1. What Money Really Is

Money serves three fundamental functions in an economy:

- A medium of exchange (a way to buy and sell);

- A unit of account (a measure of value);

- A store of value (something that preserves purchasing power over time).

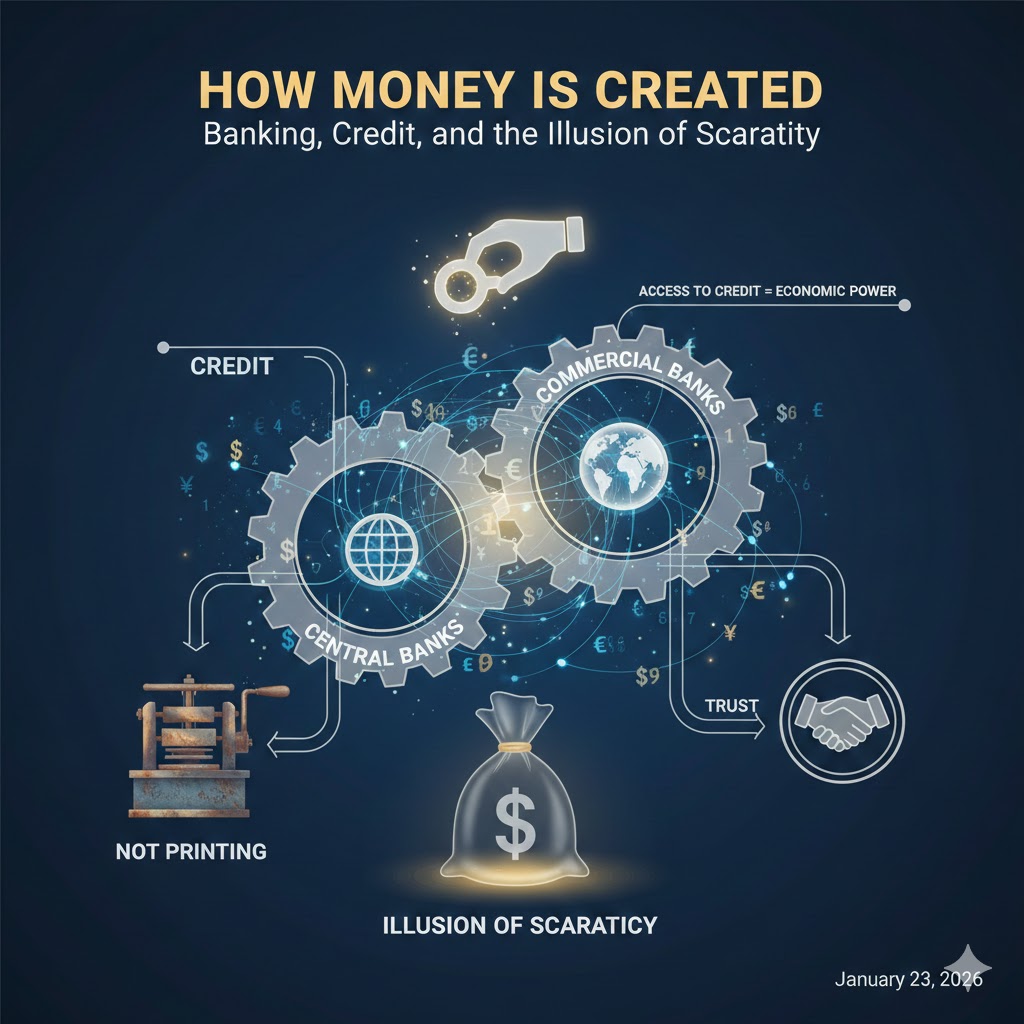

Physical money — cash and coins — is only a small fraction of the total money supply. Most money exists as account balances held at commercial banks. According to economists like Hyman Minsky and central bank research, over 90% of money in developed economies is created by commercial banks when they extend loans, not by printing new banknotes. This insight overturns the common myth that governments or central banks simply “print” all the money.

2. The Mechanics of Bank Credit Creation

When a commercial bank issues a loan, it does not take deposits and then lend them out. Instead, it creates a new deposit in the borrower’s account at the same moment the loan is made. This process increases the money supply.

For example:

- If you borrow $1,000 from a bank, the bank credits your account with a $1,000 deposit.

- At the same time, the bank records a $1,000 loan on its balance sheet.

- No physical currency needs to change hands. The bank simply creates money as a promise to repay.

This mechanism reflects the core insight of modern monetary theory and banking practice:

Loans create deposits — not the other way around.

Central banks, such as the Federal Reserve (U.S.), the European Central Bank, or the Central Bank of Nigeria, do not issue bank credit directly. Instead, they set monetary policy and regulate the banking system. They influence what banks charge in interest rates, how much capital they must hold, and how much reserves they must maintain — all of which shape how much lending banks are willing and able to do.

3. Why Physical Cash Is Only a Fraction of Money

Physical cash plays an important role in daily transactions and public confidence, but it is a tiny part of the total money supply. Most transactions — from online purchases to business transfers — occur via electronic balances.

To illustrate:

- In many advanced economies, less than 10% of the money supply exists as physical currency.

- Over 90% is digital money created by commercial banks through lending.

This is why economists like John Maynard Keynes emphasized that money cannot be understood simply by looking at coins and notes in circulation. Money, in practice, is debt — a financial claim backed by trust in the banking system and in the economy overall.

4. Trust and the Role of Institutions

Money only functions if it is trusted. Trust underpins:

- The willingness of banks to lend;

- The willingness of people and businesses to accept deposits as payment;

- The willingness of investors and governments to rely on financial institutions.

Institutions such as central banks, regulatory authorities, and courts enforce rules that preserve confidence. Without trust — in the legal system, in contract enforcement, in lenders’ solvency — credit creation shrinks and economic activity stalls.

Nobel-laureate economist Kenneth Arrow famously remarked that “virtually every commercial transaction has within itself an element of trust.” In the context of money creation, trust enables banks to issue credit and allows that credit to be accepted as money.

5. Why Access to Credit Is More Important Than Access to Cash

Physical cash is useful for small transactions, but access to credit — the ability to borrow and invest — is what drives economic growth.

Here’s why:

a. Capital Formation

Businesses need credit to invest in equipment, hire workers, and expand operations. Without access to loans, potential economic opportunities languish.

b. Consumption and Investment

Credit allows consumers and firms to smooth consumption and invest in education, technology, and infrastructure.

c. Liquidity and Economic Dynamism

Credit enables funds to flow to where they are most productive. Without credit, economies become rigid and slow.

In this sense, the ability to create or access credit determines economic power far more than the amount of cash one holds. Individuals and businesses with strong credit access can mobilize resources that would otherwise be unavailable.

6. Dispelling the “Cash Printing” Myth

A common misunderstanding is that central banks simply “print money” whenever a government needs it. In reality:

- Central banks do create base money (cash and reserves held by banks), but this is only a small share of the total money supply.

- The real expansion of money comes from commercial bank lending.

- Central banks influence lending through policy rates, reserve requirements, and regulatory oversight — they do not directly create most of the money used in everyday transactions.

This insight is crucial for understanding how economies respond to crises, how inflation emerges, and why monetary policy matters.

7. Implications for Financial Power and Wealth

Since money is mostly credit, economic power resides with those who can access and deploy credit effectively:

- Established firms and wealthy individuals typically have easier access to credit markets.

- Small businesses and low-income individuals often face barriers due to lack of collateral, weak credit histories, or higher perceived risk.

- Policy decisions about interest rates and regulatory frameworks can dramatically affect who can borrow and on what terms.

This reality helps explain why inequality persists: access to productive credit amplifies wealth, while exclusion from credit channels entrenches economic stagnation.

Conclusion

Modern money is not a static stock of printed bills. It is a dynamic, trust-based system of credit created primarily by commercial banks. Central banks play a regulatory and policy role, but the majority of money in circulation is born from lending.

Understanding this dispels the illusion that money is scarce merely because cash is hard to find. True scarcity lies in access to credit and productive investment opportunities, not in the limited supply of physical currency.

Financial literacy at this level — recognizing how money is created and who controls its creation — is foundational for making informed personal decisions and for participating intelligently in economic discourse.