Inflation Is Not Just Rising Prices: Who It Rewards and Who It Punishes

Understanding inflation as a redistribution mechanism—not merely a cost-of-living problem

Inflation is commonly described as a rise in prices. While this description is technically correct, it is economically shallow. Inflation is not merely an inconvenience at the supermarket or fuel station; it is a powerful redistribution mechanism that quietly transfers wealth across society.

Understanding inflation properly requires moving beyond consumer prices to examine who benefits, who loses, and why. When viewed through this lens, inflation is less a neutral economic outcome and more a structural force that reshapes wealth, incentives, and economic hierarchy.

1. What Inflation Really Is

At its core, inflation is a decline in the purchasing power of money. When inflation occurs, each unit of currency buys fewer goods and services than before.

Economist Irving Fisher, in The Purchasing Power of Money, emphasized that inflation affects not only prices but real economic relationships—wages, debts, savings, and contracts.

Inflation is therefore not just about prices rising; it is about money losing value unevenly across the economy.

2. Inflation as Redistribution, Not Randomness

John Maynard Keynes famously observed:

“By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens.”

This statement reveals a crucial truth: inflation does not impact everyone equally. It redistributes wealth, often without explicit political decisions or visible transfers.

Inflation operates quietly, but systematically:

- It rewards some economic positions.

- It punishes others.

- It reshapes incentives across the entire financial system.

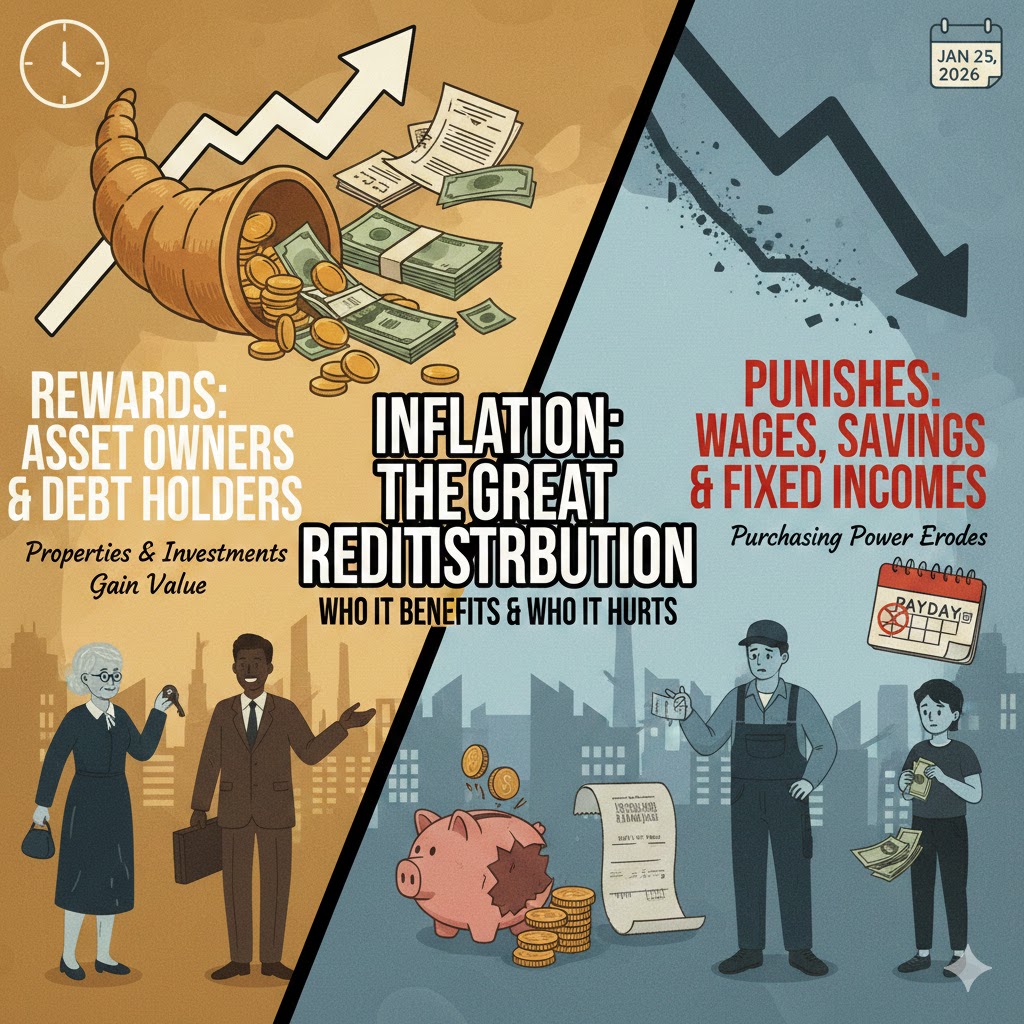

3. Who Inflation Rewards

a. Asset Owners

Inflation generally benefits those who own real and financial assets, including:

- Property

- Businesses

- Equities

- Commodities

As prices rise, the nominal value of assets often increases. Businesses can raise prices, property values adjust upward, and equities may reflect higher nominal earnings.

Economist Thomas Piketty shows that asset ownership is a primary channel through which inflation protects and often enhances wealth. Asset holders experience inflation not as loss, but as repricing.

b. Debtors

Inflation reduces the real value of debt.

A loan taken at a fixed nominal amount becomes easier to repay when the currency loses purchasing power. This is why governments with large debts often tolerate moderate inflation—it erodes debt burdens without formal default.

Milton Friedman, despite being an inflation critic, acknowledged that inflation redistributes from creditors to debtors. Borrowers repay loans with “cheaper” money.

This dynamic benefits:

- Governments

- Leveraged businesses

- Property owners with fixed-rate mortgages

c. Institutions with Pricing Power

Firms with strong market positions—monopolies, oligopolies, or essential service providers—can pass rising costs onto consumers. Inflation enhances their pricing power and preserves margins.

These firms are insulated. Workers and consumers are not.

4. Who Inflation Punishes

a. Wage Earners

Wages typically lag inflation.

While prices adjust continuously, wages are renegotiated infrequently and often under conditions of unequal bargaining power. Nobel laureate Joseph Stiglitz has repeatedly noted that labor markets do not adjust symmetrically with prices.

As a result:

- Real wages decline.

Inflation Is Not Just Rising Prices: Who It Rewards and Who It Punishes - Purchasing power erodes.

- Workers are forced to work more for less in real terms.

Hard work does not protect against inflation; ownership does.

b. Savers and Fixed-Income Earners

Inflation is particularly punitive to those who rely on:

- Cash savings

- Fixed deposits

- Pensions

- Bonds with fixed returns

When interest rates on savings are below inflation, savers experience negative real returns—their money grows numerically but shrinks economically.

This is why Keynes referred to inflation as a hidden tax on thrift.

c. The Poor and Informal Workers

Low-income households spend a larger share of income on essentials such as food, transport, and energy—items that are often most affected by inflation.

In currency-weak and informal economies, inflation compounds vulnerability:

- Income is irregular.

- Savings lack protection.

- Assets are limited or absent.

Inflation becomes regressive, disproportionately harming those least able to hedge against it.

5. Inflation and Currency Weakness

In economies with weak or depreciating currencies, inflation is often intensified by exchange rate dynamics.

Currency depreciation:

- Raises import costs

- Increases domestic prices

- Reduces global purchasing power of local incomes

An individual may earn more nominally, yet become poorer in real and international terms. This explains why inflation in developing economies often feels harsher than headline figures suggest.

Economists at the World Bank and IMF consistently emphasize that exchange rate pass-through amplifies inflation’s redistributive effects in emerging markets.

6. Why Inflation Persists

Inflation persists not only because of supply shocks or monetary policy, but because it:

- Reduces real debt burdens

- Supports asset values

- Avoids explicit redistribution through taxation

- Maintains political and financial stability in the short term

Hyman Minsky’s financial instability hypothesis suggests that inflation often emerges as systems attempt to stabilize themselves after periods of excess leverage.

Inflation is not accidental—it is often tolerated because it serves systemic functions.

7. The Illusion of Neutrality

Public discourse often treats inflation as a shared inconvenience, but this framing obscures reality. Inflation is not neutral. It is structurally biased.

Those with:

- Assets

- Leverage

- Pricing power

Are positioned to benefit.

Those dependent on:

- Wages

- Cash savings

- Fixed incomes

Are positioned to lose.

Understanding inflation is therefore not about forecasting prices, but about understanding economic positioning.

8. Financial Literacy Beyond Price Awareness

True financial literacy requires recognizing inflation as a force that reshapes wealth distribution.

This means:

- Viewing savings without yield as erosion

- Viewing debt strategically, not emotionally

- Viewing assets as protection, not luxury

- Viewing income as temporary, not foundational

Inflation teaches a hard truth: money that does not move, compounds against you.

Conclusion

Inflation is not merely rising prices—it is a silent system of redistribution. It rewards asset owners, debtors, and institutions with power, while punishing wage earners, savers, and those without economic leverage.

Understanding inflation at this structural level shifts the conversation from frustration to strategy. It clarifies why working harder is often insufficient, why saving alone can be dangerous, and why ownership and positioning matter more than effort.

Inflation does not just change prices. It changes who wins and who falls behind.