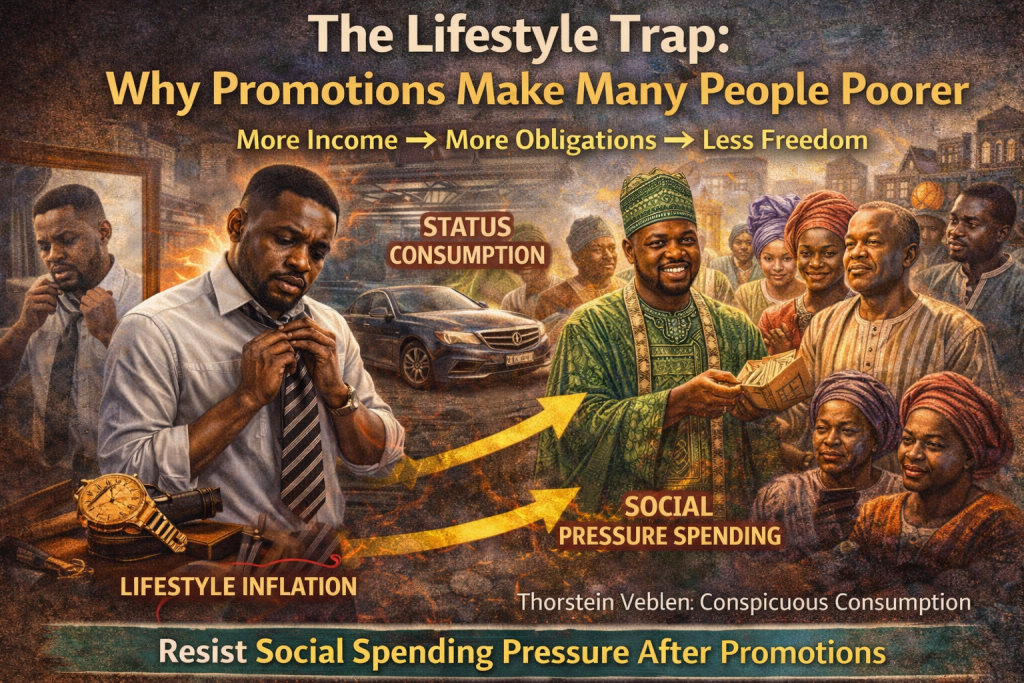

The Lifestyle Trap: Why Promotions Make Many People Poorer

A promotion is supposed to be progress.

Higher title.

Higher salary.

Higher social recognition.

Yet, paradoxically, many professionals discover that months after a raise or promotion, they feel more financially strained than before. Their income increased — but so did their obligations. Their status improved — but their freedom declined.

This is the lifestyle trap.

The core mechanism is simple:

More income → more obligations → less flexibility.

Understanding this pattern is critical, particularly in societies like Nigeria where social expectations, family responsibilities, and public displays of success carry significant cultural weight.

The Concept of Lifestyle Inflation

Lifestyle inflation occurs when an increase in income leads to a proportional — or even greater — increase in spending.

Instead of surplus income creating savings or investment capital, it creates:

- Bigger rent

- More expensive cars

- Higher social commitments

- New financial “standards”

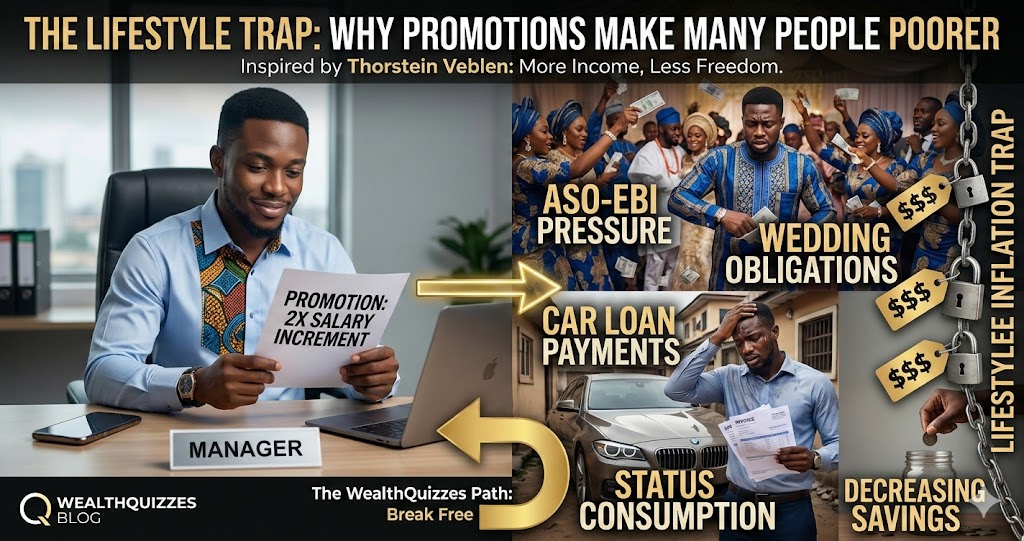

A professional earning ₦250,000 per month lives modestly. After promotion, income rises to ₦400,000. Within months:

- Rent moves from a one-bedroom to a serviced apartment.

- Transportation shifts from public transport to financed car ownership.

- Dining out becomes more frequent.

- Wardrobe upgrades become routine.

Soon, the ₦400,000 feels just as tight as the ₦250,000 once did.

The problem is not the promotion.

The problem is spending expansion.

Income Growth vs Wealth Growth

Income growth and wealth growth are not identical.

Income is a flow.

Wealth is a stock.

A salary increase improves cash flow. But if the increased flow is fully consumed by higher fixed costs, no additional wealth is accumulated.

In fact, fixed costs create fragility.

The larger your monthly obligations, the more dependent you become on uninterrupted income. This reduces bargaining power at work, increases fear of job loss, and limits risk-taking capacity.

Paradoxically, promotions can reduce freedom if spending scales too aggressively.

Status Consumption and Social Signaling

The late economist Thorstein Veblen introduced the concept of conspicuous consumption — spending money on visible goods to signal status rather than satisfy basic needs.

According to Veblen, individuals often purchase items not purely for utility but for social signaling.

In modern urban Nigeria, status consumption is highly visible:

- Luxury cars financed immediately after promotions

- Expensive wristwatches and designer clothing

- Premium phone upgrades annually

- Social media displays of lifestyle upgrades

The economic function of these purchases is often secondary. The social function dominates.

The result: financial commitments increase faster than financial resilience.

The Nigerian Social Spending Reality

Lifestyle inflation in Nigeria has an additional dimension: social obligation.

Income increases do not occur in isolation. They occur within extended family systems and social networks.

When someone is promoted, expectations often follow:

- “Now you can support more relatives.”

- “You should contribute more to family projects.”

- “You can sponsor this event.”

- “You should host this celebration.”

Cultural spending pressures are particularly visible in:

1. Weddings

Lavish ceremonies, high guest counts, expensive venues, and elaborate attire have become normalized. The financial burden often extends beyond what the couple can reasonably afford.

2. Aso-ebi Culture

Coordinated clothing for events is not inherently harmful. However, frequent participation — especially when fabrics are costly — becomes cumulative financial strain.

3. Family Expectations

A salary increase can instantly translate into school fees assistance, medical bill support, or housing contributions for extended relatives.

These pressures are rarely malicious. They are embedded in social norms.

But unmanaged, they convert income growth into obligation growth.

The Mathematics of the Trap

Consider a simplified example:

Before promotion:

- Income: ₦300,000

- Expenses: ₦220,000

- Savings: ₦80,000

After promotion:

- Income: ₦450,000

- New rent: +₦70,000

- Car loan: +₦80,000

- Increased social spending: +₦60,000

- Family obligations: +₦50,000

New expenses: ₦480,000

Despite earning ₦150,000 more, the individual now runs a deficit.

This is not theoretical. It is common.

Fixed Costs vs Variable Costs

One dangerous feature of lifestyle inflation is the conversion of variable spending into fixed obligations.

- Rent is fixed.

- Car loans are fixed.

- School fees are fixed.

- Club memberships are fixed.

Fixed costs reduce flexibility. When income drops unexpectedly, fixed costs remain.

The more fixed costs attached to your lifestyle, the less resilient you are.

Wealth is not merely income.

Wealth is the ability to survive income disruption.

Psychological Drivers Behind the Trap

Several psychological forces fuel lifestyle inflation:

1. Social Comparison

People evaluate success relative to peers. A promotion often shifts your reference group upward.

2. Identity Upgrade

A higher title can create internal pressure to “look the part.”

3. Fear of Appearing Ungrateful

Resisting social expectations may feel like arrogance or selfishness.

4. Short-Term Reward Bias

Immediate lifestyle upgrades feel satisfying. Long-term financial security feels abstract.

Without conscious discipline, these forces quietly reshape spending patterns.

Why Promotions Should Increase Freedom — Not Pressure

The financially disciplined interpretation of a promotion is different.

A raise should:

- Increase savings rate.

- Accelerate debt repayment.

- Expand investment capacity.

- Build emergency reserves.

- Create optionality.

If a promotion does not increase freedom, it has been financially neutralized.

Freedom means:

- Ability to say no to unreasonable work demands.

- Ability to withstand temporary unemployment.

- Ability to invest in new opportunities.

- Ability to relocate if necessary.

More income should buy options.

Not obligations.

Strategic Resistance to Lifestyle Inflation

Resisting the lifestyle trap requires intentional structure.

1. Freeze Core Lifestyle Temporarily

After a promotion, maintain your previous lifestyle for 6–12 months. Direct the salary increase toward savings and investments first.

2. Upgrade Selectively, Not Automatically

Improve quality of life in targeted areas rather than across all categories.

3. Separate Public Image from Financial Reality

Social perception does not build assets. Ownership does.

4. Establish a “Social Budget”

Allocate a fixed monthly amount for weddings, aso-ebi, and extended family support. Once exhausted, defer additional commitments.

5. Define Financial Goals in Writing

Clear targets (e.g., emergency fund size, investment milestones) make it easier to resist emotional spending.

The Behavioral Shift: From Reaction to Strategy

The key shift is psychological.

Instead of viewing promotions as permission to expand consumption, view them as opportunities to expand control.

You are not obligated to:

- Immediately upgrade cars.

- Increase visible spending.

- Match peers’ consumption patterns.

- Fund every social expectation.

Financial maturity includes the ability to disappoint people temporarily in order to secure long-term stability.

The Long-Term Consequence

Over decades, lifestyle inflation compounds.

Two professionals may earn identical salaries. One increases spending proportionally with each raise. The other increases investments.

After 20 years:

- One owns assets.

- The other owns obligations.

Promotions alone do not create wealth.

Retention of surplus does.

Final Reflection

The lifestyle trap is subtle because it disguises itself as progress.

You feel successful. Others treat you as successful. But internally, financial pressure intensifies.

True advancement is not visible consumption.

It is increasing control over your time, choices, and future.

When the next promotion comes, ask a different question:

“Will this increase my freedom — or just my expenses?”

That question alone can protect your financial future.