The Order of Financial Life (The Correct Sequence Nobody Teaches)

Every year, millions of people work harder financially — yet do not make progress.

They earn.

They hustle.

They invest.

They even take risks.

Yet after several years, many discover something troubling: effort increased, but security did not.

The problem is rarely laziness. It is not even primarily income level. The real problem is sequence.

Most people are not failing financially because they are doing nothing.

They are failing because they are doing the right actions in the wrong order.

In economics, order matters. A farmer does not harvest before planting. A builder does not install the roof before laying the foundation. Financial life operates under the same structural logic.

What is missing for many Nigerians — and indeed for most people globally — is a clear map.

This article presents what can be called The Real Financial Order.

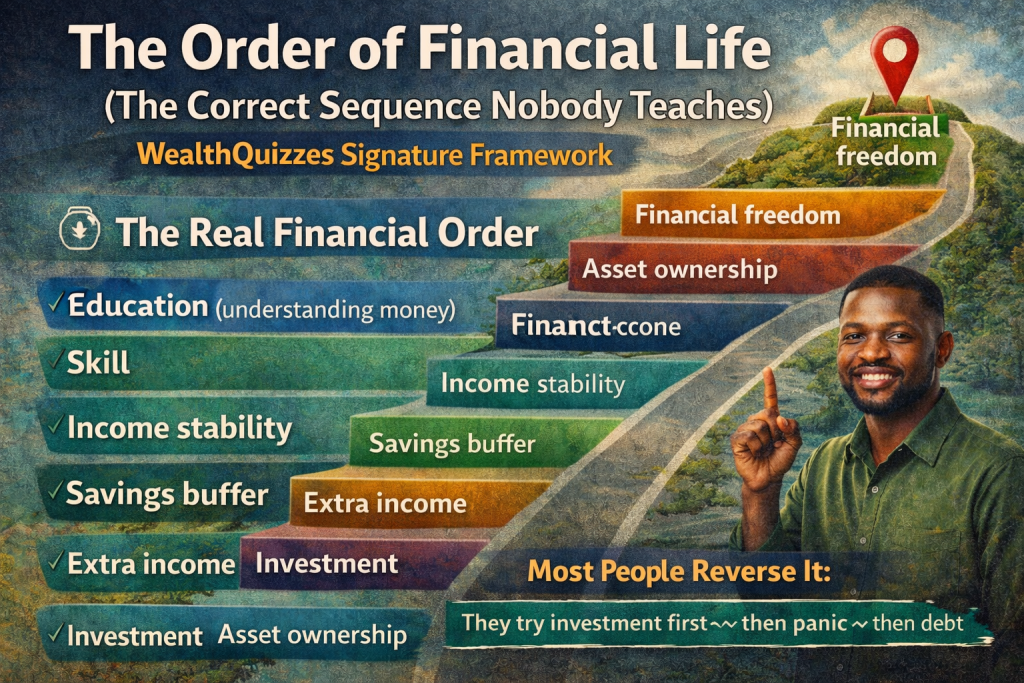

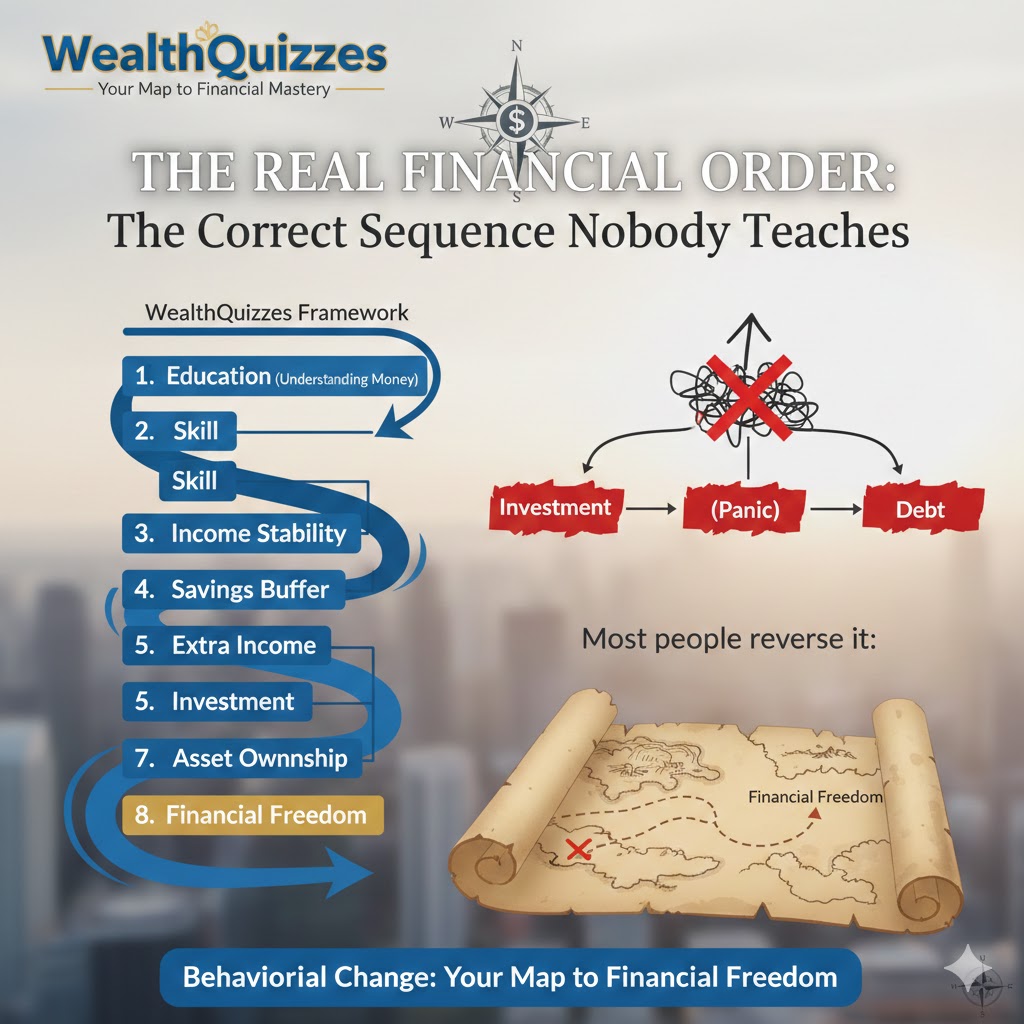

The Real Financial Order

- Education (understanding money)

- Skill

- Income stability

- Savings buffer

- Extra income

- Investment

- Asset ownership

- Financial freedom

Each stage prepares the next. Skipping one destabilizes the others.

Management thinker Peter Drucker consistently emphasized that systems fail when processes are mis-sequenced. Financial life is a system. Without order, even correct decisions produce poor outcomes.

1. Education — Understanding Money

Financial progress begins not with money, but with comprehension.

Many adults earn salaries for 20–30 years without understanding:

- the difference between income and wealth,

- the function of assets,

- the role of risk,

- or the impact of inflation.

Economist Irving Fisher demonstrated over a century ago that inflation erodes purchasing power over time. In Nigeria’s high-inflation environment, this matters profoundly. Someone who saves cash without understanding inflation is unknowingly moving backward.

Financial education does not mean studying accounting. It means grasping basic principles:

- spending vs investing

- consumption vs production

- liability vs asset

Without this, every later financial decision becomes guesswork.

2. Skill

After understanding money, the next step is the ability to generate it.

This is where many people misunderstand financial advice. They attempt to multiply money before they have reliable means of producing money.

Economist Gary Becker’s Human Capital Theory explains that knowledge and skills are forms of capital — productive capital. A skilled individual increases earning potential permanently, not temporarily.

A degree alone is not enough. A monetizable skill is required:

- writing

- technical trade

- design

- analysis

- teaching

- programming

- communication expertise

Warren Buffett repeatedly tells students:

“The best investment you can make is in yourself.”

A skill is unique among assets: it cannot be stolen, taxed directly, or wiped out by a market crash.

3. Income Stability

Income matters, but predictable income matters more.

Milton Friedman’s Permanent Income Hypothesis states that individuals make financial decisions based on expected long-term income, not temporary earnings. This explains why inconsistent income produces poor financial planning.

If income fluctuates wildly:

- savings collapse,

- investments are withdrawn early,

- debt increases.

Before attempting serious saving or investing, a person needs reliable monthly cash flow — typically from employment, contracts, or stable business revenue.

A job, therefore, is not merely a paycheck.

It is financial infrastructure.

4. Savings Buffer

This is the most ignored stage in Nigeria — and the most protective.

An emergency fund does not create wealth.

It prevents destruction.

Behavioral economist Richard Thaler demonstrated that individuals under financial pressure make significantly worse decisions. Without a savings buffer, any unexpected event forces borrowing, panic selling, or falling into scams.

A savings buffer (3–6 months of basic expenses) performs three critical functions:

- absorbs shocks,

- prevents bad decisions,

- allows long-term thinking.

This is why many people who “invested” actually lost money — they invested money they still needed.

5. Extra Income

Only after stability and safety should expansion begin.

Extra income can include:

- freelancing

- consulting

- tutoring

- small digital businesses

- specialized services

This stage is essential because it creates surplus capital.

Thomas Stanley’s research in The Millionaire Next Door revealed that wealth builders typically have multiple income streams before major investing begins. Wealth is rarely built from a single paycheck.

The purpose of extra income is not luxury.

It is investment fuel.

6. Investment

Now — and only now — investment becomes appropriate.

Investment is the purchase of assets expected to produce future income or appreciation:

- equities

- bonds

- funds

- long-term diversified portfolios

Burton Malkiel’s extensive work on market behavior shows that long-term investment works best when the investor is patient and not forced to withdraw early.

When a person invests money needed for rent, the market’s normal fluctuations become personal emergencies.

Investing requires emotional stability, and emotional stability requires financial stability.

7. Asset Ownership

Investment leads to the next stage: ownership of income-producing assets.

These may include:

- dividend-producing stocks

- rental property

- business equity

- intellectual property

- scalable digital platforms

Here is the real shift:

You are no longer earning only from labor.

You are earning from capital.

Economist Thomas Piketty describes wealth as the point where returns on capital begin to matter as much as wages. This is where true financial security begins.

8. Financial Freedom

Financial freedom does not mean never working.

It means work becomes optional.

Your living expenses can now be covered by:

- investment income

- asset income

- business distributions

Your time is no longer fully sold to survive.

What Most People Do Instead

Most people reverse the order:

They start with investment → lose money → panic → borrow → debt.

They enter crypto markets without savings.

They join Ponzi schemes without income stability.

They trade forex without skills.

The issue is not investing.

The issue is investing prematurely.

Why This Matters

Human beings naturally follow maps. When no map exists, they follow crowds.

This framework provides a map.

Instead of asking:

“Where can I invest quickly?”

A person now asks:

“Which stage am I currently in?”

That single question prevents years of financial mistakes.

Financial success is not luck.

It is sequence.

And once the sequence is correct, progress becomes predictable.