The Psychology of Money: How Emotions, Fear, and Greed Drive Financial Decisions

Money is often treated as a purely rational subject—numbers, spreadsheets, forecasts, and formulas. Yet history repeatedly shows that financial outcomes are rarely driven by logic alone. Behind every market boom, crash, personal fortune, or financial ruin lies a powerful and often underestimated force: human psychology.

Understanding money without understanding human behavior is incomplete. Intelligence, education, and technical knowledge do not guarantee wealth. In many cases, emotions—fear, greed, overconfidence, and herd behavior—play a far greater role in shaping financial decisions than raw intellect. This is the central insight of behavioral finance, a field that bridges economics and psychology to explain why people consistently make irrational financial choices.

Why Traditional Finance Got It Wrong

For decades, classical economic theory assumed that individuals are rational actors who always make decisions in their best financial interest. Markets, under this view, efficiently reflect all available information.

Reality tells a different story.

People panic during downturns, chase bubbles at market peaks, hold on to losing investments too long, and sell winning ones too early. Nobel laureate Daniel Kahneman, alongside Amos Tversky, demonstrated through decades of research that humans rely on mental shortcuts—known as cognitive biases—that systematically distort decision-making.

Markets, therefore, are not just mechanisms of price discovery; they are arenas of human emotion.

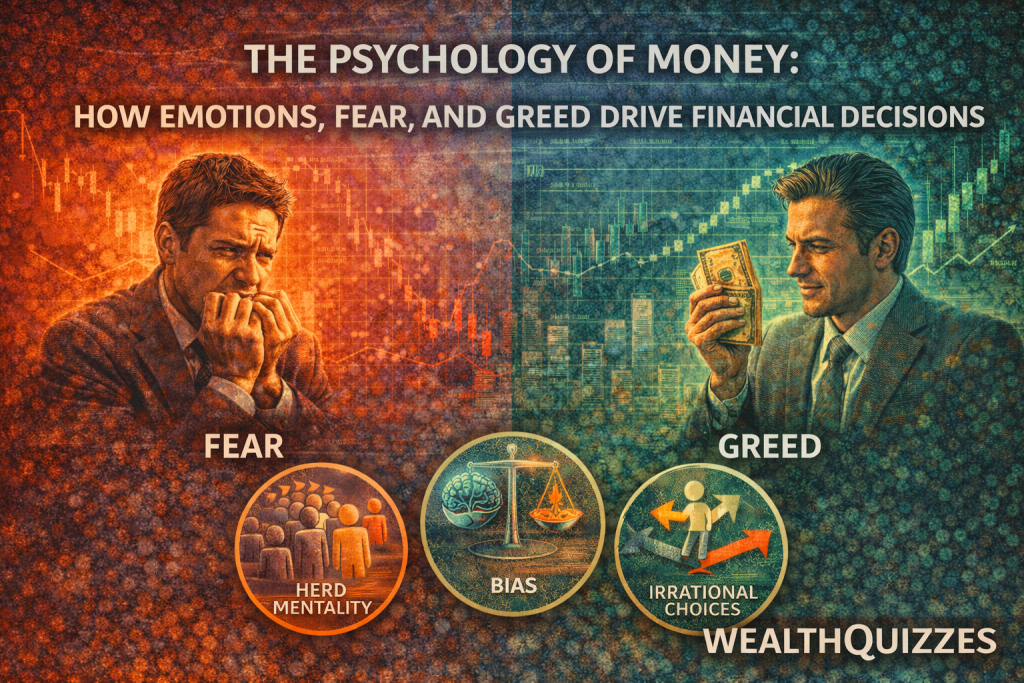

Fear: The Most Powerful Financial Emotion

Fear is evolutionarily wired into human survival instincts. In finance, however, it often becomes destructive.

Fear manifests as:

- Panic selling during market downturns

- Hoarding cash during inflationary periods

- Avoiding investment entirely after past losses

- Overreacting to negative news

Kahneman’s concept of loss aversion explains why losses feel psychologically more painful than gains feel pleasurable. As a result, investors often make irrational choices to avoid short-term losses—even when long-term data supports staying invested.

This explains why many people buy high and sell low: fear dominates at the worst possible moments.

Greed: The Fuel Behind Bubbles

If fear drives crashes, greed fuels bubbles.

Greed appears when:

- Investors chase unrealistic returns

- Risk is ignored during prolonged bull markets

- “This time is different” narratives emerge

- Leverage is used excessively

Economist Hyman Minsky famously argued that stability itself breeds instability. When markets perform well for extended periods, confidence turns into overconfidence, then speculation, and eventually recklessness.

From the dot-com bubble to the global financial crisis, greed convinces participants that rules no longer apply—until reality reasserts itself.

Cognitive Biases That Shape Financial Decisions

Behavioral finance identifies numerous biases that distort judgment. Some of the most impactful include:

Confirmation Bias

People seek information that supports existing beliefs while ignoring contradictory evidence. This leads investors to double down on poor decisions rather than reassess objectively.

Herd Mentality

Humans are social creatures. When others appear to be making money, individuals follow—often without understanding the underlying fundamentals. Herd behavior amplifies bubbles and accelerates crashes.

Overconfidence Bias

Studies show that most people believe they are above average at financial decision-making—a statistical impossibility. Overconfidence leads to excessive trading, underestimating risk, and ignoring diversification.

Anchoring

People fixate on irrelevant reference points, such as past prices or initial valuations, even when circumstances have changed.

These biases explain why intelligence and education alone do not guarantee good financial outcomes.

Why Smart People Still Make Bad Money Decisions

One of the most uncomfortable truths in finance is that high IQ does not equal financial discipline.

Highly intelligent individuals are often more susceptible to:

- Overconfidence in their analysis

- Complex rationalizations for emotional decisions

- Excessive risk-taking masked as sophistication

As investor Charlie Munger observed, “The human brain is a lot like the human egg—it has a shell that’s easy to break once it’s heated.”

Financial success depends less on brilliance and more on temperament, patience, and emotional regulation.

The Long-Term Advantage of Emotional Control

Successful investors and financially resilient individuals share common psychological traits:

- Emotional discipline during volatility

- Willingness to be patient and boring

- Acceptance of uncertainty

- Ability to delay gratification

Legendary investor Warren Buffett has repeatedly emphasized that investing is not about beating others intellectually, but about controlling oneself emotionally.

Long-term wealth is built by avoiding catastrophic mistakes, not by chasing spectacular wins.

The African Context: Emotion, Volatility, and Financial Decisions

In many African economies, economic volatility amplifies emotional decision-making. Inflation, currency instability, and policy uncertainty heighten fear and short-term thinking.

This often leads to:

- Speculative behavior as a hedge against uncertainty

- Distrust of long-term financial instruments

- Preference for tangible assets over productive investments

Improving financial outcomes therefore requires not only access to financial tools, but also psychological financial education—teaching people how to think, not just what to buy.

WealthQuizzes Perspective: Training the Financial Mind

At WealthQuizzes, financial literacy goes beyond formulas and definitions. It includes understanding how the mind interacts with money.

True financial intelligence means recognizing personal biases, resisting emotional impulses, and making decisions aligned with long-term goals rather than short-term feelings.

In a world of noise, volatility, and constant comparison, emotional discipline is a competitive advantage.

Conclusion: Wealth Is Behavioral Before It Is Mathematical

Money decisions are rarely neutral. They are shaped by fear, greed, social influence, and deeply ingrained psychological patterns. Markets may be driven by numbers, but those numbers are set by humans.

Understanding the psychology of money does not eliminate emotion—it helps manage it.

And in finance, the ability to manage yourself is often far more valuable than the ability to predict markets.

In the end, wealth is not just about how much you know—but how well you behave when it matters most.