When You Are Ready to Borrow Money — and When You Are Not

In Nigeria, borrowing money is rarely treated as a financial instrument.

It is treated as a relief system.

People borrow:

- from cooperatives,

- through salary advances,

- from friends and family,

- and increasingly from digital loan apps.

The intention is usually understandable — rent is due, a ceremony is approaching, a phone is damaged, or income came late. But the financial consequences are often severe: salary cycles collapse, anxiety rises, and repayment pressure begins to control future decisions.

The central problem is not borrowing itself.

The problem is why and when borrowing happens.

Economists do not consider debt inherently bad. In fact, modern economies run on credit. However, as financial scholar Hyman Minsky explained in his Financial Instability Hypothesis, debt becomes dangerous when it is used to support consumption rather than production. When borrowed money does not create the capacity to repay itself, financial fragility begins.

This leads to a strict and practical rule:

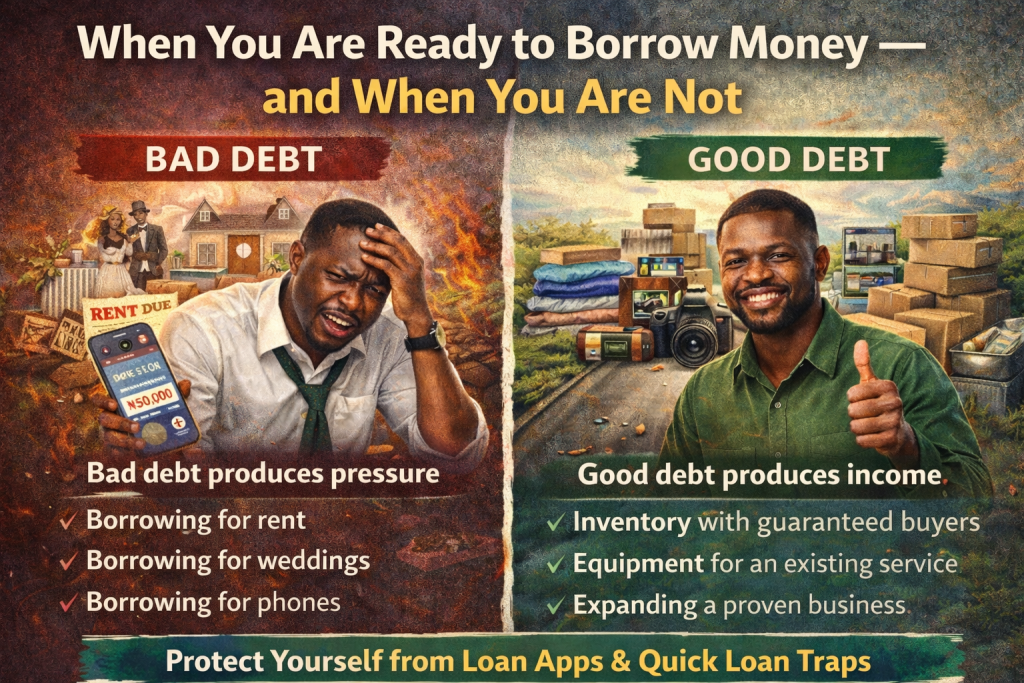

Good debt produces income.

Bad debt produces pressure.

Once this distinction is understood, most borrowing decisions become clear.

Why Borrowing Feels Necessary

In many Nigerian households, income timing is unstable:

- salaries delay,

- contract payments stall,

- business cash flow fluctuates,

- emergencies occur without warning.

Without savings buffers, borrowing becomes the default shock absorber.

Behavioral economist Richard Thaler showed that individuals under financial stress discount the future heavily — meaning immediate relief becomes more valuable than long-term stability. This is why people accept loan apps with extremely high effective interest rates. The borrower is not calculating interest; the borrower is escaping discomfort.

But debt taken to escape discomfort is almost always expensive debt.

The Three Common Emotional Borrowing Triggers

1. Social Pressure

Weddings, ceremonies, clothing expectations, and “keeping appearances” are powerful motivators. Sociologist Thorstein Veblen described this over a century ago as conspicuous consumption — spending driven by social signaling rather than utility.

Borrowing for status purchases produces no return. The event ends; the repayment remains.

2. Urgent Living Expenses

Borrowing for rent or feeding is extremely common. Yet this is the most dangerous category because it signals a structural issue: income cannot sustain basic life.

Debt cannot solve an income problem. It only postpones it.

3. Convenience Technology

Phones, gadgets, and lifestyle upgrades are increasingly financed through salary-linked loans and instant apps. Because the item is tangible, the debt feels justified. But economically, these are depreciating assets — they lose value rapidly while repayment obligations remain fixed.

Warren Buffett often distinguishes between assets and liabilities:

An asset puts money in your pocket; a liability takes money out.

A financed phone removes money monthly and produces none.

Bad Debt: Borrowing That Creates Pressure

Debt becomes harmful when repayment depends entirely on future labor rather than new income creation.

Typical bad debt examples include:

- borrowing for rent,

- borrowing for weddings,

- borrowing for clothing,

- borrowing for phones,

- borrowing to repay another loan.

Why this is dangerous:

The borrower’s future salary is already committed before it arrives. Economists call this income pre-allocation — future earnings are consumed in advance. Once multiple debts accumulate, financial flexibility disappears.

This is the mechanism behind loan-app traps. The borrower takes a small loan to solve a problem, repayment reduces next month’s cash flow, another loan becomes necessary, and a cycle forms.

The issue is not interest rate alone.

It is repayment source.

If repayment comes only from your salary, the loan is pressuring you.

Good Debt: Borrowing That Creates Income

Borrowing becomes rational only when the money increases earning capacity or produces reliable cash flow.

Examples include:

1. Inventory With Guaranteed Buyers

A food vendor who already has steady customers may borrow to purchase additional stock because sales probability is high. The inventory converts directly into revenue.

2. Equipment for an Existing Service

A photographer purchasing an additional camera, a barber buying another clipper, or a tailor acquiring an industrial sewing machine is expanding productive capacity. The tool generates income.

Economist Jean-Baptiste Say described capital goods as tools that increase productivity. When debt finances productivity, it becomes economically justifiable.

3. Expanding a Proven Business

If a trader has years of verifiable turnover and demand exceeds supply, borrowing to increase scale may be appropriate. The business has evidence, not hope.

Notice the pattern:

repayment comes from the asset, not the borrower’s salary.

This is the dividing line.

The Borrowing Readiness Test

Before taking any loan, four questions should be answered honestly:

- Does this loan directly increase my income?

- Can the activity repay the loan without my salary?

- Do I already have customers or contracts?

- If income delays, do I still have a safety buffer?

If the answer to any is “no,” the borrower is not ready.

Peter Drucker emphasized that risk is not taking action; risk is acting without understanding. Borrowing without repayment structure is not entrepreneurship — it is speculation.

Why Loan Apps Are Especially Dangerous

Digital loan platforms solve a real problem: speed. But speed removes reflection.

Because approval is instant, decision-making becomes emotional. High interest combined with short repayment cycles means the borrower must sacrifice essential expenses to meet deadlines.

The trap forms when debt begins to finance daily living rather than income creation. At that point, borrowing stops being financial leverage and becomes financial dependency.

The Proper Use of Credit

Credit should function as a tool of expansion, not survival.

Savings protects survival.

Income provides stability.

Skills create growth.

Debt should only accelerate proven productivity.

Hyman Minsky warned that financial systems become unstable when borrowers rely on new debt to service old debt. This applies not only to nations and banks but also to individuals.

The Behavioral Shift

Instead of asking:

“Where can I get a quick loan?”

The correct question becomes:

“What will repay this loan?”

If the answer is “my salary,” reconsider.

If the answer is “a productive activity already working,” then borrowing may be justified.

Final Principle

Borrowing is neither good nor bad by itself.

It is a multiplier.

If your financial structure is weak, debt multiplies stress.

If your financial structure is strong, debt multiplies opportunity.

Understanding this single distinction can prevent years of financial strain — and protect many Nigerians from falling into cycles that begin with relief but end with pressure.