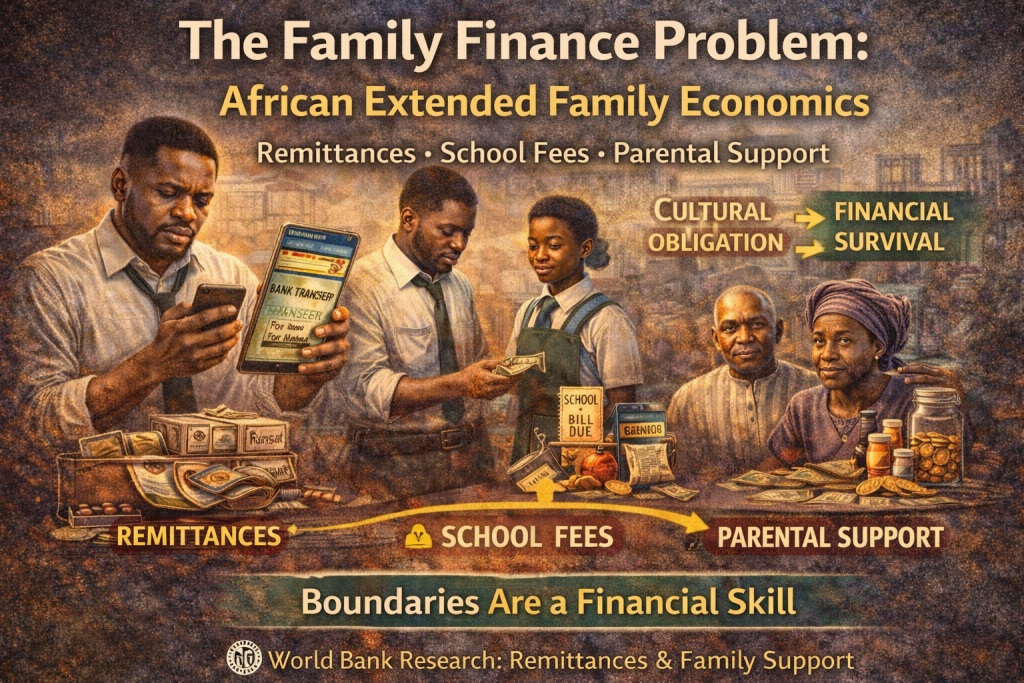

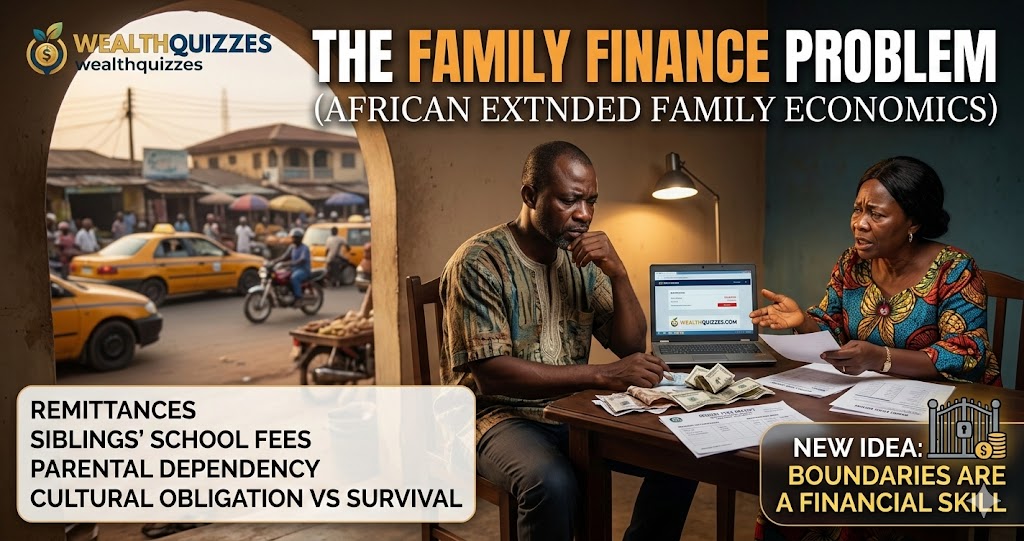

The Family Finance Problem: African Extended Family Economics

Across many African societies, financial life is rarely an individual affair. Income, resources, and responsibilities are deeply embedded in the extended family structure. While this system has historically provided social protection and community resilience, it also creates complex financial pressures for many working adults today.

Professionals, civil servants, entrepreneurs, and mid-career workers across Africa—particularly in countries like Nigeria—often face a silent economic burden: the obligation to financially support relatives. These responsibilities may include sending remittances to extended family members, paying siblings’ school fees, caring for aging parents, or responding to emergency requests from relatives.

Although such support is culturally valued and socially expected, it also produces what can be described as the family finance problem—a situation in which personal financial stability becomes difficult because resources are continuously redistributed within the extended family network.

Understanding this issue requires examining the intersection between culture, economics, and financial behavior.

The Economics of Remittances

One of the most visible forms of extended family financial support is remittances—the transfer of money from one family member to another, often across geographic distances.

Research by the World Bank shows that remittances are a major component of household income in many developing economies. While global discussions often focus on international remittances from migrants abroad, domestic remittances within countries are equally significant.

In African economies, urban workers frequently send money back to relatives living in rural areas or smaller towns. These transfers support basic necessities such as:

- Food and household supplies

- Medical expenses

- School fees for younger siblings

- Rent or building projects

- Emergency family needs

From a development economics perspective, remittances perform an important social function: they act as informal insurance systems where family members support one another during financial hardship.

However, for the individual sending the money, these obligations can create substantial financial strain—especially when income growth does not keep pace with the number of dependents.

Siblings’ School Fees and the “First Success Syndrome”

A common pattern in African families occurs when one child achieves educational or professional success earlier than others. Once employed, that individual often becomes responsible for supporting the educational expenses of younger siblings.

This phenomenon is sometimes described informally as “first success syndrome.”

The expectation operates quietly but powerfully:

- The eldest employed child pays siblings’ tuition.

- They may cover accommodation, books, and feeding allowances.

- In some cases, the responsibility extends to cousins or other relatives.

While the motivation is noble—helping others climb the same ladder—it can delay the financial progress of the supporting sibling. Instead of saving, investing, or purchasing assets, much of their income becomes redirected toward family obligations.

Over time, this can significantly slow personal wealth accumulation.

Parental Dependency in Aging Societies

Another major financial responsibility arises from parental dependency.

In many African societies, formal pension systems are weak or inconsistent. As a result, parents often rely heavily on their children for financial support during retirement.

Unlike Western models where elderly care may be supported by social welfare systems, African family structures function as the primary safety net.

Children may therefore be responsible for:

- Monthly allowances for parents

- Medical bills

- House renovations

- Food and utilities

- Caregiving during illness

From a moral and cultural standpoint, these obligations are widely respected. Respect for parents and elder care are deeply embedded values.

However, from a financial planning perspective, this creates what economists sometimes call intergenerational financial pressure—where one generation’s economic responsibilities significantly shape the financial capacity of the next.

Cultural Obligation vs Financial Survival

The real challenge is not the existence of family obligations but the scale and structure of those obligations.

In many cases, support begins informally and gradually expands. A small monthly transfer may grow into multiple commitments:

- Supporting parents

- Paying a sibling’s tuition

- Funding a cousin’s business idea

- Contributing to family ceremonies

- Responding to emergency requests

Over time, these obligations can consume a significant portion of income.

For many working professionals, the result is a confusing financial paradox:

They earn reasonable salaries but still struggle to save, invest, or achieve financial independence.

The issue is rarely irresponsibility. Instead, it is the cumulative impact of extended family economics.

The Hidden Financial Risk: Unstructured Giving

A major problem arises when financial support occurs without structure or boundaries.

Unstructured giving often leads to:

- unpredictable requests for money

- emotional pressure during family emergencies

- difficulty refusing relatives

- inconsistent personal budgeting

Because the financial support system is informal, there are rarely clear limits.

Development economists studying remittance behavior note that while family transfers improve welfare at the household level, they can also reduce individual capital accumulation for the sender if not carefully managed.

In simple terms: supporting everyone today can make it harder to build stability for tomorrow.

Boundaries Are a Financial Skill

A crucial but often overlooked concept in personal finance is that boundaries are a financial skill.

Financial boundaries do not mean abandoning family responsibilities. Rather, they mean creating structured systems of support that protect both generosity and financial sustainability.

Healthy financial boundaries may include:

1. Budgeted Family Support

Instead of responding to requests randomly, individuals can allocate a fixed percentage of income for family support each month.

For example:

- 10–15% of income reserved for family assistance

- Once that budget is exhausted, additional requests wait until the next month.

This approach ensures support remains consistent without destroying personal financial plans.

2. Prioritizing Education Over Consumption

Structured support can focus on investments that improve long-term outcomes, such as:

- education

- vocational training

- health emergencies

Rather than funding lifestyle expenses or repeated short-term requests.

3. Avoiding the “Single Provider Trap”

Another risk occurs when one family member becomes the sole financial provider for many relatives.

Encouraging shared responsibility among siblings can distribute financial pressure more evenly across the family network.

4. Separating Emergencies from Expectations

A genuine medical emergency is different from routine financial requests.

Creating categories of support helps maintain clarity:

- emergency support

- education support

- general assistance

Each category can have its own limits.

Balancing Culture and Financial Independence

The extended family system is one of Africa’s greatest social strengths. It promotes solidarity, mutual support, and resilience during difficult times.

However, modern economic realities—urban living costs, inflation, and job instability—require new financial strategies to sustain this tradition without sacrificing personal financial stability.

Structured giving allows individuals to remain supportive family members while still building their own economic future.

Without such balance, many professionals find themselves trapped in a cycle where income increases but wealth never accumulates.

A Smarter Model for Family Support

The solution is not abandoning family responsibility. It is managing it intelligently.

Financially sustainable family support involves:

- clear boundaries

- planned contributions

- prioritizing long-term empowerment over short-term consumption

- protecting personal savings and investment goals

When approached with structure and discipline, extended family support can remain a source of strength rather than financial strain.

Final Thought

The reality of African extended family economics is that financial success rarely belongs to one person alone. It often lifts an entire network of relatives.

But generosity without structure can quietly erode financial stability.

The most powerful lesson is simple but transformative:

Helping family is noble. Helping family sustainably is wisdom.

Learning to create financial boundaries is not selfish—it is a necessary skill for building both personal stability and lasting family support.