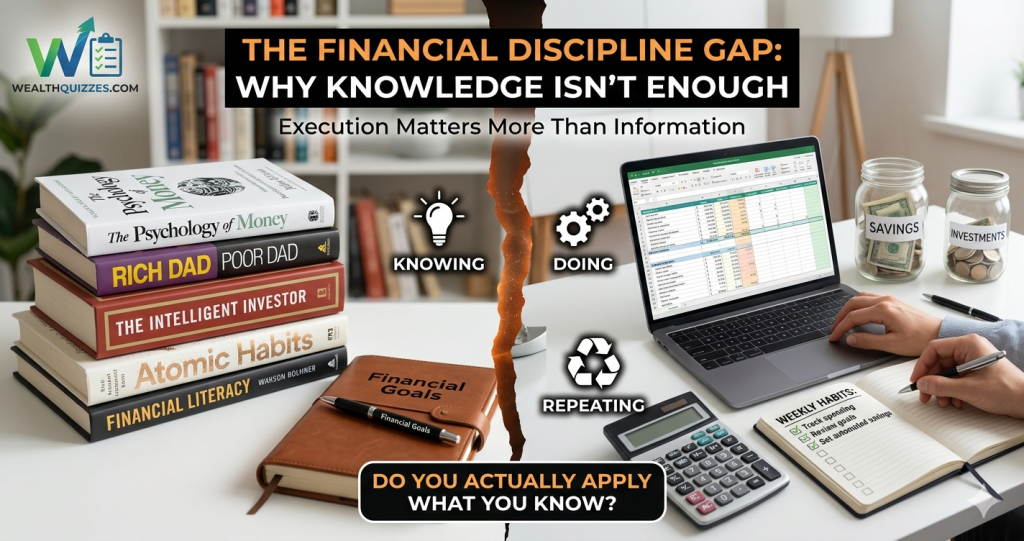

The Financial Discipline Gap: Why Knowledge Isn’t Enough

Bridging the Divide Between What You Know and What You Actually Do

Introduction: The Knowledge Illusion

We live in an era of unprecedented access to financial information.

You can:

- Watch countless finance videos

- Read books on wealth creation

- Follow experts online

- Learn budgeting, saving, and investing strategies

Yet, despite all this knowledge, many people are still:

- Broke

- Financially inconsistent

- Stuck in the same patterns

This raises a critical question:

If people know what to do, why aren’t they doing it?

The answer lies in a fundamental but often ignored gap:

The Financial Discipline Gap

The Core Truth

Core Idea: Execution matters more than information

Mindset Shift: Knowing → Doing → Repeating

Knowing what to do financially is not enough.

Wealth is built through consistent execution—not information.

Understanding the Financial Discipline Gap

The Financial Discipline Gap is:

The difference between what you know and what you consistently do

You may know:

- You should save

- You should invest

- You should avoid unnecessary spending

But:

- You don’t always act on it

- You don’t sustain it

The Knowledge Trap

Many people fall into what can be called:

The knowledge trap

They:

- Consume more information

- Learn more strategies

- Feel more prepared

But do not:

- Implement

- Practice

- Repeat

As Peter Drucker famously stated:

“Knowledge has to be improved, challenged, and increased constantly, or it vanishes.”

But even more importantly:

Knowledge without application is useless.

The Financial Discipline Gap: Why Knowledge Isn’t Enough

Why Knowledge Fails Without Discipline

1. Behavioral Inconsistency

Human behavior is not naturally consistent.

As Daniel Kahneman explains, people often act irrationally, driven by:

- Emotions

- Biases

- Short-term thinking

This leads to:

- Saving today, spending tomorrow

- Planning ahead, then abandoning it

2. Emotional Overrides

Financial decisions are rarely purely logical.

They are influenced by:

- Mood

- Stress

- Social pressure

This creates a gap between:

- What you know

- What you actually do

3. Lack of Systems

Without structure:

- Discipline relies on willpower

And willpower is:

- Limited

- Inconsistent

The Role of Habits in Financial Success

Financial discipline is not about:

- Occasional good decisions

It is about:

Repeated behavior over time

As James Clear explains:

“You do not rise to the level of your goals. You fall to the level of your systems.”

Habit Formation: The Missing Link

1. Small Actions, Big Results

Wealth is built through:

- Small, consistent actions

Not:

- One-time decisions

2. Automation of Behavior

Habits remove:

- Decision fatigue

- Emotional interference

3. Consistency Over Intensity

It is better to:

- Save small amounts consistently

Than:

- Save large amounts occasionally

The Discipline Equation

Financial success follows a simple pattern:

Knowledge + Execution + Consistency = Results

Remove execution, and:

- Knowledge becomes irrelevant

Why People Struggle with Financial Discipline

1. Overconfidence in Knowledge

People assume:

- Knowing is enough

2. Lack of Immediate Reward

Saving and investing:

- Do not provide instant gratification

3. Environment and Influence

Spending culture:

- Encourages consumption

- Discourages discipline

4. No Accountability

Without tracking:

- Behavior becomes inconsistent

The Nigerian Context: Why the Gap Is Wider

In Nigeria:

- Financial education is increasing

- Awareness is growing

But:

- Economic pressure is high

- Social spending expectations are strong

This creates:

A wide gap between knowledge and practice

The Real Cost of the Discipline Gap

1. Financial Stagnation

Despite knowing what to do:

- Progress is minimal

2. Repeated Mistakes

You:

- Learn lessons

- Then repeat the same errors

3. Lost Opportunities

Knowledge not applied:

- Produces no results

4. Frustration

You feel:

- Aware but stuck

Closing the Gap: From Knowing to Doing

1. Simplify Your Financial System

Avoid complexity.

Focus on:

- Basic, repeatable actions

2. Automate Discipline

Set up:

- Automatic savings

- Investment plans

3. Track Your Behavior

Measure:

- Spending

- Saving

- Progress

4. Build Financial Habits

Start with:

- Small, consistent actions

5. Reduce Decision Points

The fewer choices you make:

- The more consistent you become

The Power of Repetition

Discipline is not built through:

- Motivation

It is built through:

Repetition

The Identity Shift

To sustain discipline, you must shift identity:

From:

- “I know about money”

To:

- “I am financially disciplined”

The Real Transformation

When you close the discipline gap:

You move from:

- Knowledge → Action

- Intention → Execution

- Inconsistency → Stability

The Hard Truth

Most people are not financially stuck because:

- They lack knowledge

They are stuck because:

They do not apply what they know.

Conclusion: Execution Is Everything

In finance:

- Knowledge is potential

- Action is power

- Consistency is wealth

Because:

You don’t build wealth by knowing—you build it by doing.

Final Thought

Before you learn another financial strategy, ask yourself:

“Am I applying what I already know?”

Because the gap between knowing and doing is where most financial failure lives.

👉 Do you actually apply what you know? Find out on WealthQuizzes