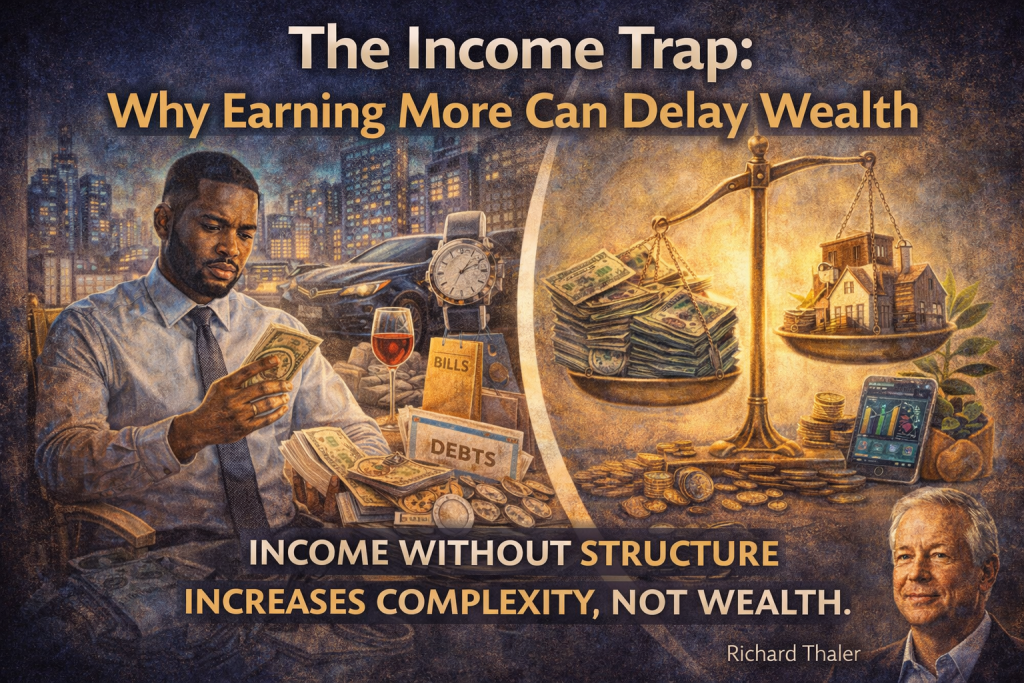

The Income Trap: Why Earning More Can Delay Wealth

For many people, the path to financial success appears straightforward: earn more money. Promotions, salary increases, and additional income streams are widely seen as the primary solution to financial stress and instability.

Yet, a closer look at real-world financial outcomes reveals a surprising paradox:

Many high earners are not wealthy. In fact, some are financially fragile despite earning significantly more than average.

This phenomenon is known as the income trap—a situation where increasing income does not translate into increasing wealth, and may, in some cases, delay it.

Understanding this trap requires a shift in perspective: from focusing on how much you earn to understanding how income is structured, allocated, and deployed.

Income Growth vs Wealth Growth

At first glance, income and wealth appear closely related. However, they are fundamentally different concepts.

- Income is the flow of money earned over time.

- Wealth is the accumulation of assets that generate value independently of your effort.

The assumption that higher income automatically leads to wealth ignores a critical factor: behavioral and structural responses to income increases.

In practice, when income rises, spending often rises with it.

This phenomenon is widely recognized in economics as lifestyle inflation.

The Mechanics of Lifestyle Expansion

Lifestyle inflation occurs when individuals increase their spending as their income grows.

For example:

- a salary increase leads to upgrading accommodation

- additional income results in more frequent dining out

- a promotion encourages purchasing more expensive clothing or gadgets

- social expectations increase with perceived status

These changes are often gradual and appear justified. After all, earning more seems to permit a higher standard of living.

However, over time, these incremental upgrades create a new baseline of expenses.

The result is that the financial margin does not expand—even though income has increased.

The Income Illusion

At the heart of the income trap is what can be described as the income illusion:

the belief that earning more automatically solves financial problems.

This illusion leads to several dangerous assumptions:

- “Once I earn more, I will start saving.”

- “Higher income will give me financial freedom.”

- “My current financial stress is purely an income problem.”

In reality, income often magnifies existing financial habits.

If a person struggles with poor financial structure at a lower income level, a higher income may simply amplify those inefficiencies.

Instead of solving the problem, more money can make it less visible—until financial pressure eventually reappears.

Why High Earners Still Live Paycheck-to-Paycheck

One of the most striking manifestations of the income trap is the persistence of paycheck dependency among high earners.

Despite earning substantial incomes, many individuals remain financially vulnerable. Their expenses are so closely aligned with their earnings that any disruption—job loss, delayed payment, or unexpected cost—creates immediate financial stress.

This condition arises from several structural issues:

1. Fixed Cost Expansion

As income increases, individuals often take on higher fixed expenses:

- larger rent or mortgage commitments

- car loans

- school fees

- lifestyle obligations

Fixed costs reduce flexibility. Once established, they are difficult to adjust quickly.

2. Social Status Pressure

Higher income often comes with increased social expectations.

People may feel compelled to maintain a certain image:

- attending expensive events

- participating in social spending

- supporting extended networks

This pressure can silently consume a significant portion of income.

3. Lack of Asset Allocation

Many high earners focus on consumption rather than asset creation.

Income is spent rather than invested in:

- income-generating assets

- scalable opportunities

- long-term financial instruments

Without asset accumulation, financial independence remains out of reach—regardless of income level.

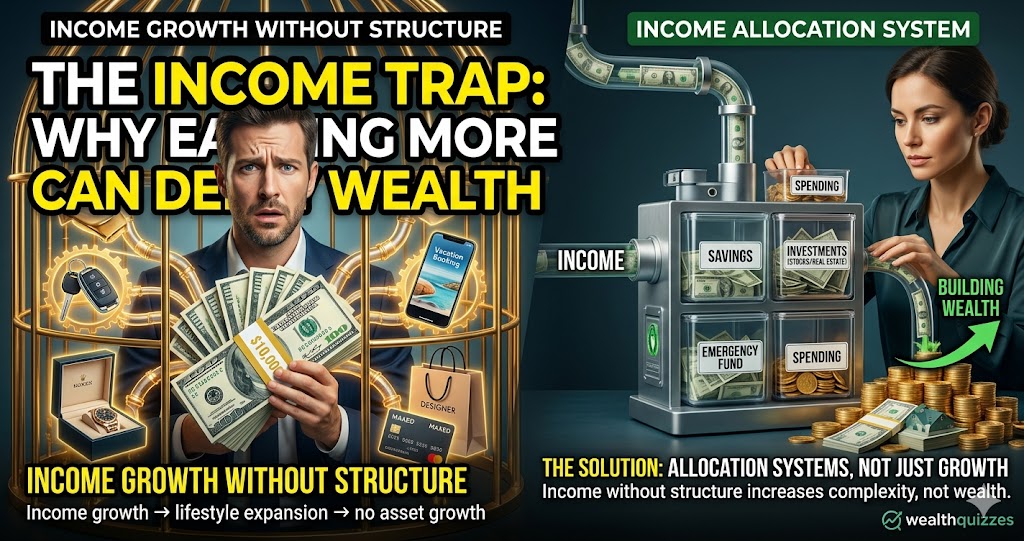

The Structural Problem: Income Without Allocation

The core issue behind the income trap is not income itself, but lack of structure in how income is used.

Income without a clear allocation system leads to:

- uncontrolled spending

- inconsistent savings

- absence of investment

- financial stagnation

As complexity increases with higher income, the absence of structure becomes more damaging.

This is why the key principle is:

Income without structure increases complexity, not wealth.

Lessons from Behavioral Economics

Behavioral economics provides valuable insight into why this pattern is so common.

Researchers such as Richard Thaler have shown that individuals do not always make rational financial decisions. Instead, they rely on mental shortcuts and habits.

One relevant concept is mental accounting—the tendency to treat money differently depending on its source or context.

For example:

- salary increases may be perceived as “extra money” and spent more freely

- bonuses may be used for discretionary spending rather than investment

These behaviors reinforce the income trap by preventing disciplined allocation of additional income.

From Earning to Structuring: The Real Shift

Escaping the income trap requires a fundamental shift in financial thinking.

Instead of focusing primarily on earning more, individuals must focus on structuring income effectively.

This involves intentional allocation across key financial priorities:

1. Consumption

Essential living expenses should be controlled and proportionate to income.

2. Savings

A portion of income should be consistently set aside to create financial stability.

3. Investment

Funds must be directed toward assets that generate future income or appreciate in value.

4. Growth

Investment in skills, knowledge, or opportunities that increase earning potential.

When income is structured in this way, increases in earnings translate into increases in financial capacity, not just lifestyle expansion.

Building Income Allocation Systems

The most effective way to ensure proper financial structure is through systems, not intentions.

Systems reduce the need for daily decision-making and enforce consistency.

Examples include:

- automatic transfers to savings and investment accounts

- fixed percentage allocations for different financial goals

- separate accounts for spending, saving, and investing

- predefined rules for handling income increases

These systems transform financial management from a reactive process into a controlled strategy.

Redefining Financial Progress

One of the most important mindset shifts is redefining what progress looks like.

Instead of measuring success by:

- salary level

- lifestyle upgrades

- visible consumption

progress should be measured by:

- asset growth

- financial stability

- reduced dependency on income

- increased control over time and choices

This shift aligns financial behavior with long-term outcomes rather than short-term appearances.

Final Thought

The belief that earning more leads to wealth is one of the most persistent myths in personal finance.

While income is essential, it is not sufficient.

Without structure, higher income can create greater complexity, higher obligations, and deeper financial dependence.

The real path to wealth lies not in how much you earn, but in how effectively you convert income into assets and long-term value.

As behavioral insights from Richard Thaler suggest, financial outcomes are shaped not just by income, but by how individuals manage and allocate their resources.

In the end, escaping the income trap requires a simple but powerful shift:

Stop focusing only on earning more.

Start focusing on building systems that make your money work for you.