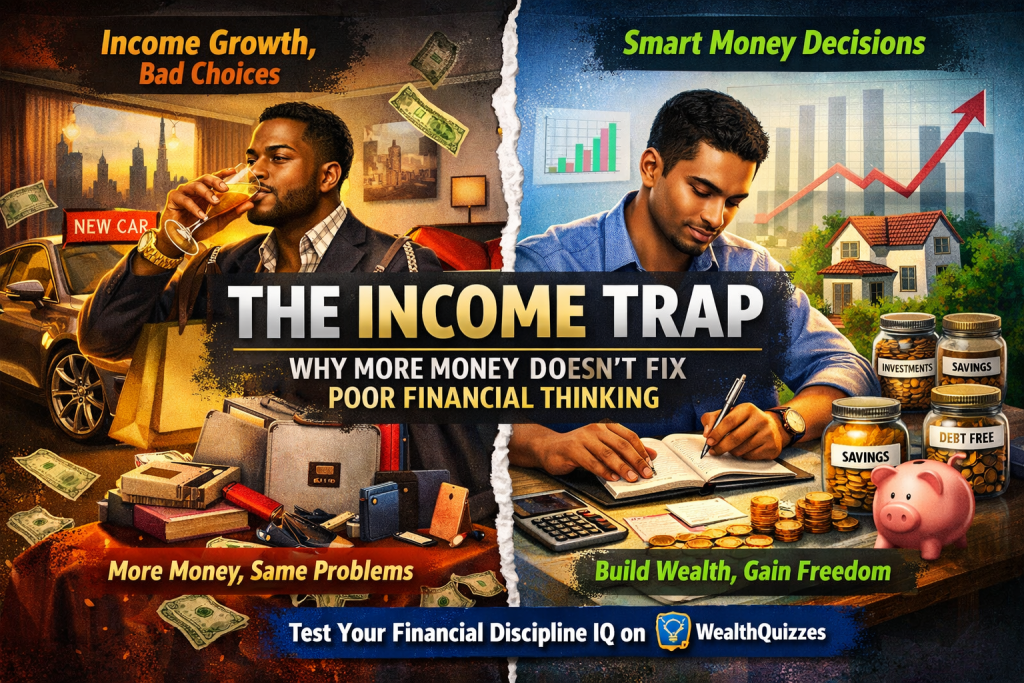

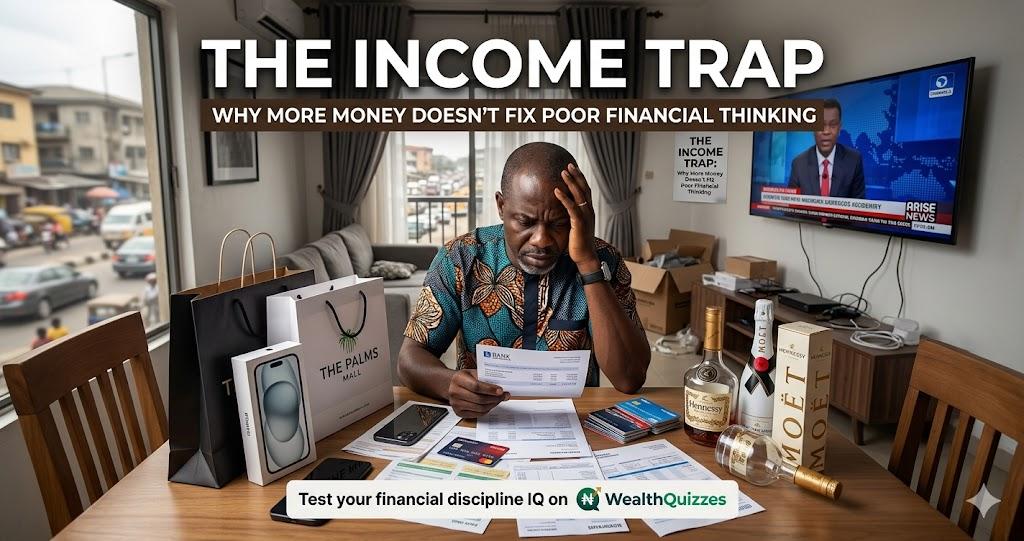

The Income Trap: Why More Money Doesn’t Fix Poor Financial Thinking

Introduction: The Dangerous Assumption

There is a widely accepted belief in modern society—especially among young professionals—that earning more money automatically leads to financial stability. It sounds logical: if income increases, then financial stress should reduce.

But reality tells a different story.

Across Nigeria and globally, many individuals experience salary increases, promotions, or new income streams—yet remain financially stuck, constantly waiting for the next paycheck, unable to build meaningful wealth.

This paradox is not an income problem.

It is a thinking problem.

Core Truth: Income growth without discipline does not solve financial problems—it amplifies them.

The Income Trap Explained

The “income trap” occurs when increased earnings are matched—or exceeded—by increased spending, leaving the individual no better off financially.

This phenomenon is closely tied to what economists and financial experts call lifestyle inflation (or lifestyle creep)—the tendency to increase spending as income rises. (Moneycentral)

In practical terms:

- You earn more

- You upgrade your lifestyle

- Your expenses rise

- Your financial position remains unchanged

Sometimes, it even gets worse.

As financial analysts have observed, lifestyle inflation can lead individuals to live paycheck-to-paycheck despite earning more, because increased expenses offset income gains. (Moneycentral)

Why More Money Doesn’t Fix Poor Financial Thinking

1. Income Amplifies Existing Habits

Money does not change behavior—it reveals and magnifies it.

- If you are disciplined with ₦100,000, you will likely be disciplined with ₦500,000

- If you are careless with ₦100,000, you will likely be reckless with ₦500,000

This aligns with behavioral finance principles: financial outcomes are largely driven by habits, not income levels.

In other words:

Income is a multiplier. It scales whatever financial behavior already exists.

2. Lifestyle Inflation: The Silent Wealth Killer

One of the most dangerous consequences of increased income is lifestyle inflation.

Defined simply, it is the tendency for spending to rise alongside income, often turning luxuries into perceived necessities over time. (Wikipedia)

In the Nigerian context, this is extremely visible:

- Upgrading from shared apartments to expensive solo apartments

- Switching from public transport to daily ride-hailing

- Increasing frequency of dining out and social spending

- Subscribing to multiple digital services

What starts as “rewarding yourself” becomes a permanent cost structure.

Financial experts warn that without a plan, higher discretionary income naturally leads to higher consumption, making it harder to save or invest. (Business Post Nigeria)

3. Salary Upgrades vs Spending Upgrades

Here lies the core mistake:

Most people upgrade their lifestyle faster than they upgrade their financial systems.

Let’s break this down.

Scenario A: Strategic Thinker

- Salary increases by ₦100,000

- ₦60,000 goes to savings/investments

- ₦40,000 improves lifestyle

Scenario B: Emotional Spender

- Salary increases by ₦100,000

- ₦90,000 goes to lifestyle upgrades

- ₦10,000 (or nothing) is saved

Over time, the gap between these two individuals becomes massive—not because of income, but because of allocation discipline.

Financial guidance often recommends that a significant portion of any income increase should be redirected toward future-oriented uses like savings, investments, or debt reduction. (altbank)

4. The Psychological Drivers Behind the Trap

The income trap is not just financial—it is deeply psychological.

a. Social Comparison

Humans naturally compare themselves with others.

In Nigeria, this manifests in:

- Weddings

- Fashion

- Cars

- Social media lifestyle displays

This aligns with classical economic theory, particularly the concept of conspicuous consumption, introduced by Thorstein Veblen—where people spend money to signal status rather than create value.

b. Emotional Spending

Increased income creates a sense of entitlement:

- “I deserve this”

- “I’ve worked hard”

This leads to impulsive financial decisions disguised as rewards.

c. Lack of Financial Identity

Many individuals do not have a clear answer to:

“What is my financial goal?”

Without this clarity, income is directionless—and directionless money is easily spent.

The Nigerian Reality: More Naira, Less Value

The income trap is even more dangerous in Nigeria due to economic conditions.

Recent economic data shows that although Nigerians are spending more in nominal terms, the actual value of that spending has declined due to inflation. (Businessday NG)

In simple terms:

- You may be earning more

- You may even be spending more

- But your real financial position may not be improving

Additionally, behavioral studies indicate that Nigerians’ spending habits are strongly influenced by social interactions, economic perception, and environmental pressures. (OAPub)

This means:

Financial decisions are not purely logical—they are socially and psychologically driven.

The Illusion of Progress

One of the most dangerous aspects of the income trap is that it feels like progress.

You see:

- Better clothes

- Better phone

- Better apartment

But beneath that surface:

- No investments

- No emergency fund

- No assets

This creates what can be described as “cosmetic wealth”—a lifestyle that looks successful but lacks financial substance.

Breaking Free from the Income Trap

Escaping this trap requires a deliberate shift in thinking and behavior.

1. Adopt the “Wealth Allocation” Mindset

Before spending new income, decide:

- What percentage goes to savings?

- What goes to investments?

- What goes to lifestyle?

2. Delay Lifestyle Upgrades

Not every increase in income should lead to an immediate lifestyle change.

Discipline means:

Just because you can afford it doesn’t mean you should buy it.

3. Build Systems, Not Willpower

Relying on self-control alone is weak.

Instead:

- Automate savings

- Separate accounts

- Create spending rules

4. Define Your Financial Identity

Ask yourself:

- Am I a consumer or a builder?

- Am I optimizing for appearance or for freedom?

The Real Mindset Shift

The fundamental shift is this:

More income does not create wealth. Better decisions do.

Wealth is not determined by:

- How much you earn

But by:

- How much you keep

- How well you grow it

- How consistently you apply discipline

Conclusion: The Hard Truth

The income trap is not obvious. It does not feel like a problem.

In fact, it often feels like success.

But if your expenses rise as fast as your income, then:

You are not moving forward—you are running in place.

Final Thought (Conversion Hook)

Before your next salary increase or new income stream, ask yourself:

“Will this money change my life—or just my lifestyle?”

If you want to find out how disciplined you really are with money:

👉 Test your financial discipline IQ on WealthQuizzes

Because the real difference between the rich and the struggling is not income—

It is thinking.