Why Financial Discipline Fails Without Systems

Financial advice often emphasizes discipline as the cornerstone of success. Spend less, save more, avoid unnecessary expenses—these principles are repeated so frequently that they appear sufficient on their own.

Yet, in practice, many disciplined individuals still struggle financially.

They create budgets, set goals, and commit to better habits—only to find themselves slipping back into old patterns. The issue is not a lack of intention or even effort. It is something deeper and more structural.

Discipline, by itself, is unreliable. Systems are what make discipline sustainable.

To understand why financial discipline often fails, we must examine how human behavior actually works—and why relying on willpower alone is an unstable strategy.

The Limits of Discipline

Discipline is often treated as a constant trait: something you either have or lack. In reality, discipline is variable.

It fluctuates based on:

- stress levels

- mental fatigue

- environment

- emotional state

- daily demands

This means that even highly disciplined individuals will experience periods of reduced self-control.

Behavioral research by Roy Baumeister introduced the concept of ego depletion, suggesting that self-control is a limited resource that diminishes with use.

In practical terms, this implies:

- making many decisions reduces mental energy

- resisting temptation becomes harder over time

- consistency becomes difficult without structural support

This explains why relying solely on discipline often leads to inconsistency.

Why Budgets Fail

Budgeting is one of the most common financial tools. It is also one of the most frequently abandoned.

At its core, a budget requires continuous:

- tracking

- decision-making

- restraint

- adjustment

While effective in theory, budgeting places a heavy burden on discipline.

Every spending decision becomes a test of willpower.

For example:

- choosing whether to spend or save

- deciding whether a purchase fits within a category

- adjusting plans when unexpected expenses arise

Over time, this constant decision-making leads to fatigue.

The behavioral economist Richard Thaler has shown that individuals often deviate from rational plans due to behavioral biases and mental shortcuts.

Budgets fail not because they are flawed, but because they depend too heavily on consistent human behavior.

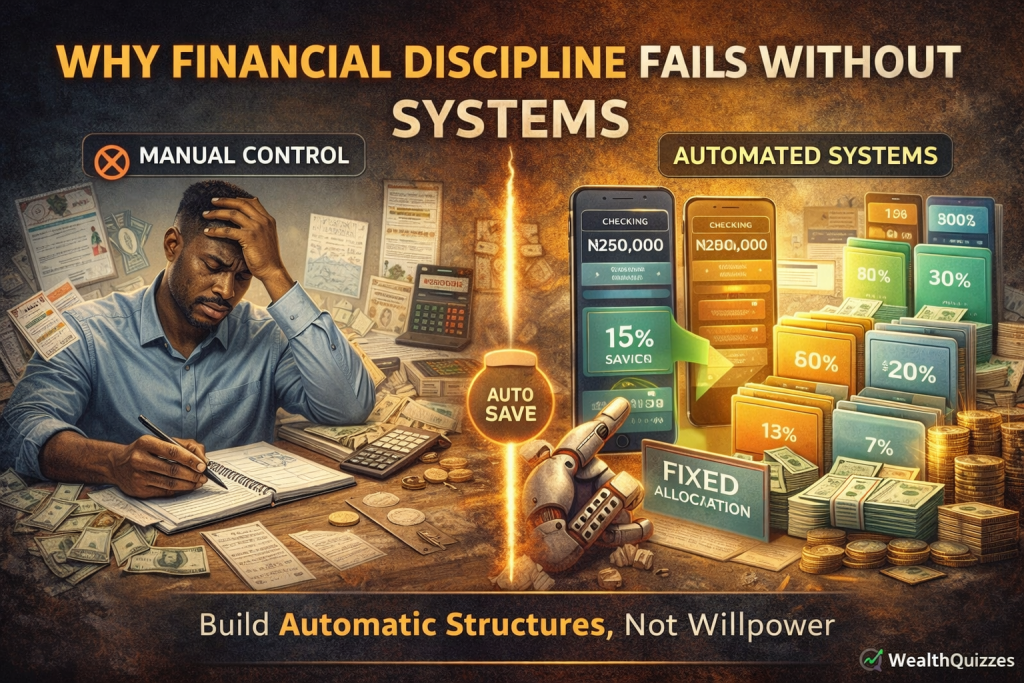

The Problem with Manual Control

Manual financial management requires ongoing attention and effort.

This includes:

- transferring money into savings

- tracking expenses

- deciding how much to invest

- adjusting allocations

Each of these actions requires a conscious decision.

The more decisions required, the higher the probability of:

- delay

- avoidance

- inconsistency

This is where many financial plans break down.

Not because people do not know what to do—but because the system requires them to continuously do it.

Systems: The Missing Link

A system is a structure that operates with minimal ongoing decision-making.

In finance, systems are designed to:

- automate behavior

- reduce reliance on willpower

- ensure consistency

- simplify decision-making

The key advantage of systems is that they remove the need to repeatedly choose the right action.

Instead of asking, “Should I save this month?” the system ensures that saving happens automatically.

Automation vs Willpower

Automation is one of the most effective ways to implement financial systems.

Examples include:

- automatic transfers to savings accounts

- scheduled investments

- fixed bill payments

- standing orders for contributions

Automation transforms financial discipline from an active process into a passive one.

The individual no longer needs to remember, decide, or resist.

The system handles it.

This aligns with insights from Daniel Kahneman, who distinguished between fast (automatic) and slow (deliberate) thinking.

By embedding financial actions into automatic processes, individuals reduce the need for slow, effortful decision-making.

Core Financial Systems That Work

To build sustainable financial discipline, individuals must implement simple but effective systems.

1. Auto-Saving System

A fixed percentage of income is automatically transferred to savings immediately upon receipt.

This ensures that saving is prioritized, not optional.

2. Separate Accounts Structure

Different accounts are used for:

- spending

- savings

- investments

This creates clear boundaries and reduces the risk of mixing funds.

3. Fixed Allocation Model

Income is divided into predefined percentages for:

- living expenses

- savings

- investments

- personal spending

This removes the need to decide allocation repeatedly.

4. Automated Investment System

Regular, scheduled investments ensure consistent asset growth without requiring constant intervention.

5. Expense Friction Mechanisms

Introduce barriers to impulsive spending, such as:

- limiting access to discretionary funds

- avoiding stored payment methods

- using separate cards for different purposes

These systems create a financial environment where the default behavior is the correct behavior.

Systems Reduce Decision Fatigue

One of the most powerful benefits of systems is the reduction of decision fatigue.

As daily decisions accumulate, mental energy declines. This leads to poorer choices, especially in areas requiring discipline.

By automating financial actions, systems:

- reduce the number of decisions required

- conserve mental energy

- increase consistency

- improve long-term outcomes

Instead of making hundreds of small decisions, individuals rely on a few well-designed structures.

From Intentions to Infrastructure

The shift from discipline to systems represents a deeper transformation:

- from intention to execution

- from effort to structure

- from inconsistency to reliability

Financial success becomes less about trying harder and more about designing better systems.

This aligns with a broader principle in productivity and behavioral science:

Environment and structure often outperform willpower.

Behavioral Shift: Designing for Success

The most important change is how individuals approach financial management.

Instead of asking:

“How can I be more disciplined?”

The more effective question is:

“What system can make this automatic?”

This shift reduces reliance on motivation and increases reliance on structure.

Final Thought

Financial discipline is important—but it is not enough.

As insights from Roy Baumeister, Richard Thaler, and Daniel Kahneman suggest, human behavior is inherently inconsistent.

Relying on willpower alone is a fragile strategy.

Systems, on the other hand, provide stability. They operate regardless of mood, energy, or circumstances.

They turn good intentions into consistent action.

In the end, financial success is not about being perfectly disciplined.

It is about building systems that make discipline unnecessary.

Because when the system is right,

the results follow automatically.