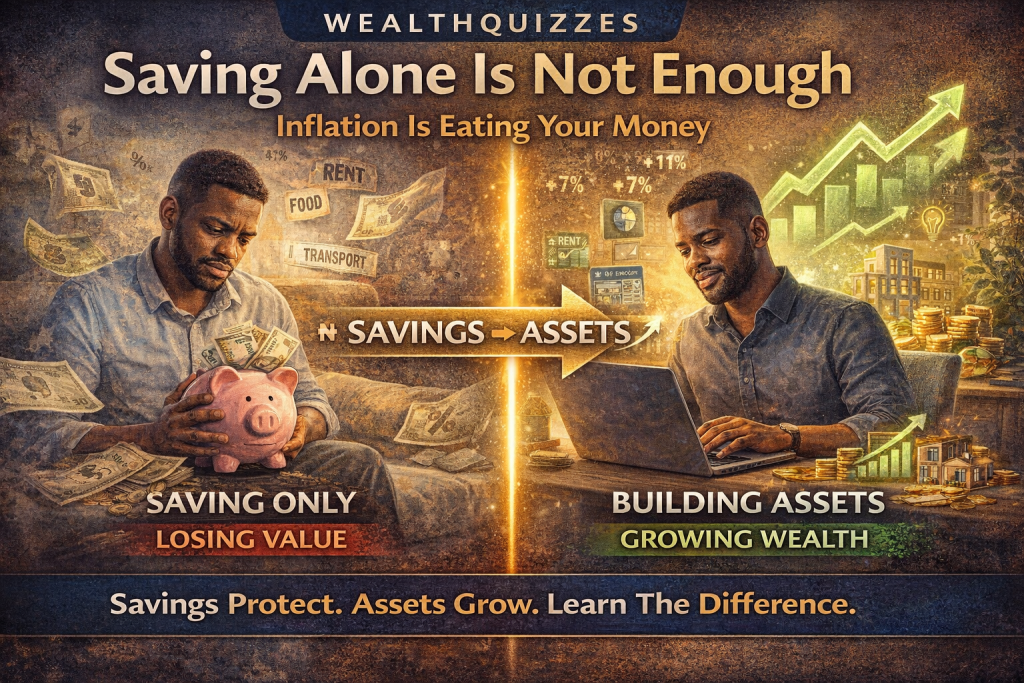

Why Saving Alone Will Not Make You Financially Secure

For many individuals seeking financial stability, the most common advice is simple and widely accepted: save your money.

Save a portion of your salary. Avoid unnecessary expenses. Build a reserve for the future.

While this advice is fundamentally sound, it is often misunderstood in one critical way:

Saving alone is not enough to guarantee financial security.

In fact, an over-reliance on saving—without a broader financial strategy—can quietly limit long-term wealth and, in some cases, reduce financial resilience.

To understand why, we must examine the limitations of saving and the economic forces that erode its effectiveness over time.

The Role of Saving: Protection, Not Growth

Saving plays an essential role in personal finance. It provides:

- emergency protection

- short-term stability

- psychological security

- liquidity for unexpected events

Without savings, individuals are vulnerable to financial shocks such as medical emergencies, job loss, or sudden expenses.

However, saving performs a defensive function. It preserves money; it does not significantly grow it.

This distinction is crucial.

Savings protect you. Assets grow you.

Confusing these two roles leads to a financial strategy that is safe in the short term but ineffective in the long term.

Inflation: The Silent Erosion of Savings

One of the most important reasons saving alone is insufficient is inflation.

Inflation refers to the general increase in prices over time, which reduces the purchasing power of money.

The economist Milton Friedman famously described inflation as a monetary phenomenon, emphasizing its persistent and systemic nature.

In practical terms, inflation means:

- ₦100,000 today will buy less in the future

- the cost of food, rent, and transportation increases over time

- the real value of saved money declines if it does not grow

For example, if inflation averages 15% annually in an economy, money kept in cash or low-interest accounts effectively loses value each year.

Even if the nominal amount remains the same, the real value decreases.

This creates a paradox:

A person who diligently saves but does not invest may actually become poorer in real terms over time.

The Limits of Salary-Based Savings

Another constraint is the limited capacity of salary-based savings.

Most individuals save from earned income, which is inherently constrained by:

- salary levels

- employment conditions

- time availability

- economic environment

There is a ceiling to how much one can save from income alone.

Even with disciplined saving, the accumulation process is slow. Consider:

- saving ₦50,000 monthly results in ₦600,000 annually

- over five years, this amounts to ₦3 million (excluding inflation effects)

While this is commendable, it may not be sufficient to achieve major financial goals such as:

- property ownership

- business expansion

- financial independence

The limitation is structural.

Savings grow linearly. Wealth grows exponentially.

The Missing Link: Assets

To overcome the limitations of saving, individuals must transition from saving money to deploying money into assets.

An asset is anything that generates income, appreciates in value, or both.

Examples include:

- business investments

- dividend-paying stocks

- rental property

- digital income streams

- skills that generate additional income

Unlike savings, assets have the capacity to:

- grow over time

- generate recurring income

- outpace inflation

- compound value

This is the mechanism through which financial security—and eventually financial independence—is achieved.

Why Many People Stop at Saving

Despite the clear advantages of asset-building, many individuals remain stuck at the saving stage.

This is often due to:

1. Fear of Loss

Investing introduces uncertainty. People fear losing their hard-earned money.

2. Lack of Financial Education

Understanding how to identify and manage assets requires knowledge that many people have not been exposed to.

3. Cultural Conditioning

In many environments, saving is emphasized more than investing.

Saving is seen as responsible; investing is sometimes viewed as risky.

4. Short-Term Focus

Immediate financial needs often take priority over long-term growth strategies.

These factors create a comfort zone around saving, even when it is insufficient for long-term security.

The Transition: From Saving to Purposeful Allocation

The solution is not to stop saving, but to redefine the role of saving.

Savings should serve as a foundation, not a destination.

A structured financial approach involves three stages:

1. Build an Emergency Buffer

This provides stability and reduces financial stress.

2. Maintain Liquidity for Short-Term Needs

Ensure access to funds for predictable expenses.

3. Deploy Surplus into Assets

Convert excess savings into income-generating or appreciating assets.

This transition transforms saving from a passive activity into an active strategy.

The Concept of Purchasing Power

To fully understand why saving alone is insufficient, it is important to consider purchasing power—the amount of goods and services money can buy.

The economist John Maynard Keynes emphasized the importance of real values (adjusted for inflation) rather than nominal values.

A person may accumulate savings over time, but if those savings do not keep pace with inflation, their purchasing power declines.

This means:

- more money is required to maintain the same standard of living

- financial goals become harder to achieve

- long-term security becomes uncertain

Assets, on the other hand, have the potential to preserve or increase purchasing power.

Building a Balanced Financial Strategy

A sustainable financial strategy balances protection and growth.

Saving alone emphasizes protection.

Asset-building introduces growth.

The combination of both creates resilience.

A practical approach may include:

- allocating a percentage of income to savings

- directing another portion to investments

- continuously reinvesting returns

- increasing asset allocation as income grows

This creates a system where money is not just stored—it is working.

Behavioral Shift: From Hoarding to Deploying

The most important change is behavioral.

Instead of asking:

“How much can I save?”

The more effective question is:

“How can I make my savings grow?”

This shift moves individuals from a defensive mindset to a strategic mindset.

Saving becomes intentional, with a clear purpose: to fund future asset creation.

Final Thought

Saving is an essential first step in financial stability. It provides security, discipline, and a foundation for future growth.

But it is not the final step.

As economic realities such as inflation and income limitations demonstrate, saving alone cannot deliver long-term financial security.

As insights from economists like Milton Friedman and John Maynard Keynes suggest, understanding the difference between nominal value and real value is critical.

Money that is not growing is quietly losing value.

The path to true financial security lies in a simple but powerful progression:

Save → Convert → Grow

Because in the end,

savings protect you—but assets build your future.