The Capital Allocation Mindset: Why Wealthy People Think in Percentages

How Financial Destiny Is Determined Less by Income—and More by Allocation

Introduction: The Hidden Difference Between the Rich and Everyone Else

Most people focus heavily on:

- How much money they earn

Wealthy people focus heavily on:

- Where money goes

This distinction appears simple, but it changes everything.

Two people can earn the same income and end up with completely different financial outcomes.

One person:

- Builds assets

- Expands investments

- Increases long-term wealth

The other:

- Remains trapped in financial pressure

- Lives paycheck to paycheck

- Experiences little lasting growth

The difference is often not:

- Intelligence

- Luck

- Talent

The difference is:

Allocation.

Wealthy individuals understand a principle that many people ignore:

Financial destiny is determined less by income size and more by capital allocation efficiency.

The Core Truth

Core Idea: Allocation determines financial destiny

Angle: Capital efficiency

Money behaves differently depending on:

- How it is distributed

- What it is assigned to do

- Whether it is consumed or deployed strategically

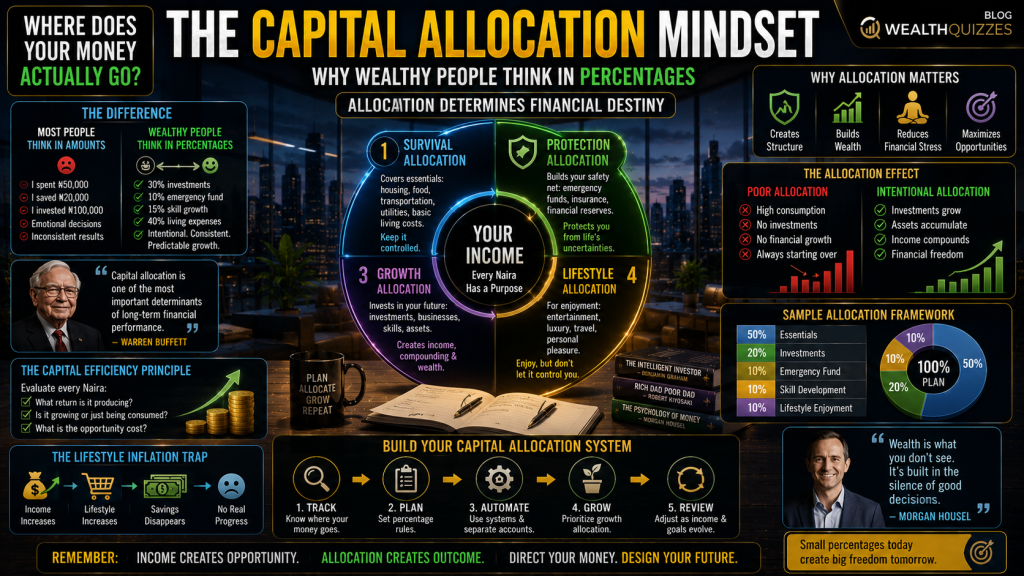

The Percentage Thinking Mindset

Most financially struggling people think in:

- Amounts

Wealth builders think in:

- Percentages

Example of Amount Thinking

- “I spent ₦50,000.”

- “I saved ₦20,000.”

- “I invested ₦100,000.”

Example of Percentage Thinking

- “30% goes to investments.”

- “10% goes to emergency reserves.”

- “15% funds skill growth.”

- “40% covers living expenses.”

Why This Matters

Percentage thinking creates:

- Structure

- Scalability

- Predictability

- Financial control

Amount thinking creates:

- Emotional spending

- Inconsistency

- Financial drift

Insight from Authority

As Warren Buffett consistently demonstrates through his investment philosophy:

Capital allocation is one of the most important determinants of long-term financial performance.

Buffett’s success has never depended merely on earning money, but on:

- Deploying capital efficiently over time.

What Is Capital Allocation?

Capital allocation is:

The strategic distribution of financial resources toward priorities that maximize long-term value.

Every naira you earn is assigned somewhere.

The real question is:

Is it being allocated intentionally—or emotionally?

Every Allocation Creates a Future

Money allocation is not merely spending.

It is:

Future construction.

Every financial decision creates consequences.

Money directed toward:

- Consumption

Produces: - Temporary satisfaction

Money directed toward:

- Assets

Produces: - Future cash flow and wealth expansion

Insight from Authority

As Peter Drucker famously emphasized:

What gets measured gets managed.

Percentage allocation creates measurable financial behavior.

The Four Major Allocation Categories

Most effective wealth systems allocate capital across four major areas.

1. Survival Allocation

This covers:

- Food

- Housing

- Transportation

- Utilities

- Basic living costs

Important Principle:

Survival spending should remain controlled.

Why?

Because uncontrolled lifestyle expansion destroys capital efficiency.

2. Protection Allocation

This includes:

- Emergency funds

- Insurance

- Financial reserves

Purpose:

Protection prevents financial collapse during crises.

3. Growth Allocation

This is where wealth acceleration begins.

Examples include:

- Investments

- Businesses

- Skill acquisition

- Asset accumulation

Growth allocation creates:

- Future earning capacity

- Compounding opportunities

4. Lifestyle Allocation

This covers:

- Entertainment

- Luxury spending

- Social consumption

- Personal enjoyment

Important:

Lifestyle spending is not inherently bad.

The problem occurs when:

Lifestyle consumes capital meant for growth.

The Capital Efficiency Principle

Wealthy individuals constantly evaluate:

“What return is this money producing?”

This is capital efficiency thinking.

Every naira is assessed based on:

- Long-term value

- Productivity

- Opportunity cost

Example:

Two people receive:

- ₦500,000

Person A allocates toward:

- Gadgets

- Fashion

- Social spending

Person B allocates toward:

- Investments

- Skill systems

- Business expansion

Five years later:

The outcomes may differ dramatically.

Why?

Because:

Allocation compounds over time.

The Nigerian Context: Why Allocation Matters More Than Ever

Nigeria’s economic environment includes:

- Inflation pressure

- Currency instability

- Rising living costs

This means:

Poor allocation decisions become increasingly expensive.

Without strategic allocation:

- Income growth may never translate into wealth growth.

Many people experience:

- Salary increases

But: - No meaningful financial progress

Why?

Because increased income is often absorbed immediately into:

- Lifestyle inflation

Insight from Authority

As Morgan Housel explains:

Wealth is what you don’t see.

Real wealth is often:

- Unspent capital

- Accumulated assets

- Deferred consumption

The Lifestyle Inflation Trap

One of the greatest enemies of capital allocation is:

Lifestyle drift.

This occurs when:

Income increases lead immediately to:

- Bigger expenses

- Higher consumption

- More status spending

Result:

Financial pressure remains constant despite higher earnings.

The wealthy often behave differently.

Instead of scaling consumption aggressively, they scale:

- Investments

- Assets

- Ownership

Percentage Thinking Creates Stability

When finances operate through percentages:

- Decisions become less emotional

- Systems become more predictable

Example Framework

A structured income allocation model may include:

- 50% essentials

- 20% investments

- 10% emergency reserves

- 10% skill development

- 10% lifestyle enjoyment

The exact percentages may differ.

The critical issue is:

Intentional structure.

The Psychology of Allocation

Allocation reflects:

- Priorities

- Identity

- Long-term thinking

Financial chaos often reveals:

- Lack of systems

- Reactive decision-making

- Absence of planning

Strong allocation systems create:

- Discipline

- Financial clarity

- Reduced anxiety

The Difference Between Earners and Builders

Earners focus mainly on:

- Generating income

Builders focus on:

- Directing capital strategically

This is why:

Some high earners remain financially unstable while moderate earners gradually accumulate wealth.

The Role of Opportunity Cost

Every allocation decision carries:

Opportunity cost.

Money spent today cannot simultaneously:

- Compound tomorrow

Insight from Authority

Economist Thomas Sowell famously observed:

There are no solutions. There are only trade-offs.

Every allocation choice involves trade-offs between:

- Present consumption

And: - Future growth

Building Your Capital Allocation System

Step 1: Track Current Allocation

Ask:

- Where does my money actually go?

Step 2: Create Percentage Rules

Assign:

- Specific percentages to priorities

Step 3: Automate Allocation

Use:

- Separate accounts

- Automatic transfers

- Investment systems

Step 4: Prioritize Growth Allocation

Ensure part of every income cycle funds:

- Assets

- Investments

- Future cash flow systems

Step 5: Review and Optimize

Allocation systems should evolve as:

- Income grows

- Responsibilities change

- Financial goals expand

The Identity Shift

To build wealth effectively, you must move from:

- “I spend money as it comes”

To:

“I deploy capital intentionally according to structure.”

The Real Transformation

Capital allocation changes:

- Financial behavior

- Wealth trajectory

- Long-term outcomes

Eventually:

Money stops disappearing randomly and begins:

Building measurable financial progress.

The Hard Truth

Many people do not have an income problem.

They have:

An allocation problem.

Conclusion: Allocation Shapes Destiny

Wealth is rarely built accidentally.

It is built through:

- Structured financial behavior

- Deliberate allocation

- Capital efficiency

Income creates opportunity.

But:

Allocation determines outcome.

The people who build lasting wealth are usually not those who merely earn the most.

They are:

The people who consistently direct money toward productive purposes over long periods of time.

Final Thought

Ask yourself honestly:

“Where does my money actually go every month?”

Because the difference between financial pressure and financial freedom is often not how much you earn—

It is:

How efficiently you allocate what you already have.

👉 Where does your money actually go? Find out on WealthQuizzes