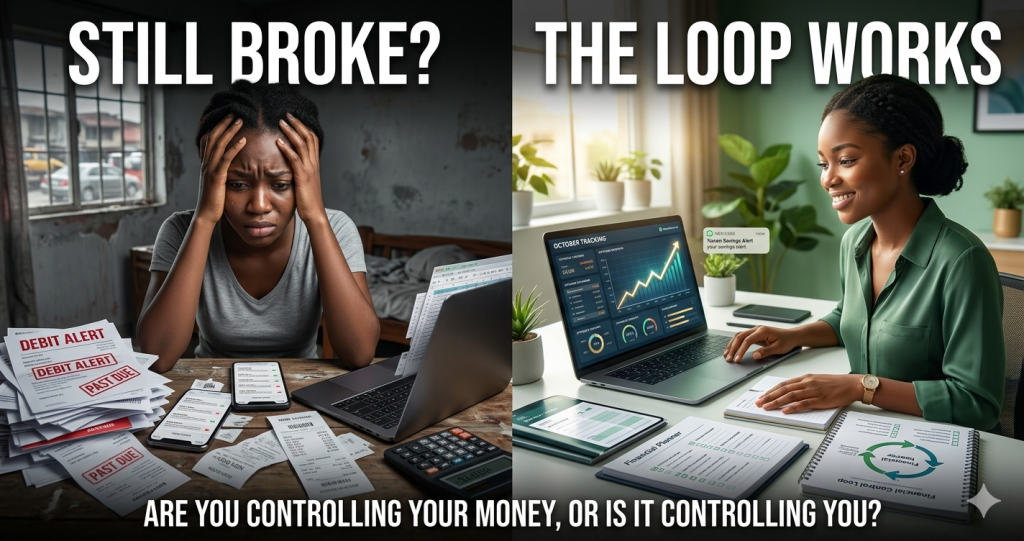

The Financial Control Loop: How to Track, Adjust, and Optimize Money Monthly

Turning Your Finances from Passive Drift into Active, Measurable Progress

Introduction: Why Most People Don’t Know Where Their Money Goes

A common financial complaint cuts across income levels:

- “My money just disappears.”

- “I don’t know how I spent so much this month.”

- “I earn, but I don’t see progress.”

These are not income problems. They are control problems.

At the center of this issue is a missing system—specifically:

A repeatable process for tracking, reviewing, and improving financial behavior.

This process is what we call:

The Financial Control Loop

The Core Truth

Core Idea: What gets tracked gets improved

Mindset Shift: Passive → Active control

Money left unmonitored will always drift toward:

- Convenience

- Impulse

- Immediate gratification

Money that is tracked and reviewed becomes:

- Structured

- Intentional

- Optimized

What Is the Financial Control Loop?

The Financial Control Loop is a monthly feedback system that ensures your money is:

- Tracked – You know exactly what happened

- Analyzed – You understand why it happened

- Adjusted – You improve future decisions

Why a “Loop” Matters

A one-time budget is not enough.

A static plan fails because:

- Life changes

- Expenses fluctuate

- Behavior evolves

A loop ensures:

Continuous correction and improvement

Insight from Authority

As W. Edwards Deming famously stated:

“You can’t improve what you don’t measure.”

This principle, widely applied in business and engineering, is equally powerful in personal finance.

The Three Stages of the Financial Control Loop

🔍 1. Tracking: Knowing the Truth About Your Money

The Objective:

Gain visibility

What to Track:

- Total income

- Fixed expenses (rent, utilities)

- Variable expenses (food, transport, lifestyle)

- Savings and investments

The Problem Most People Have

They rely on:

- Memory

- Bank alerts

- Rough estimates

Why This Fails

Human recall is:

- Incomplete

- Biased

- Emotionally filtered

The System Approach

Use tools such as:

- Expense trackers

- Spreadsheets

- Budgeting apps

Insight from Authority

As Peter Drucker emphasized:

“What gets measured gets managed.”

Result of Proper Tracking:

- Awareness of spending patterns

- Identification of waste

- Clarity on financial behavior

📊 2. Analysis: Understanding What Went Wrong (or Right)

The Objective:

Interpret the data

Key Questions to Ask:

- Where did most of my money go?

- What expenses were necessary?

- What expenses were avoidable?

- Did I follow my allocation plan?

What Analysis Reveals:

- Spending leaks

- Emotional triggers

- Poor allocation decisions

Common Discovery

Many people find that:

- Small daily expenses accumulate into significant losses

Insight from Authority

As Morgan Housel explains:

Financial success is driven more by behavior than knowledge.

Without Analysis:

- Mistakes repeat

- Progress stalls

🔧 3. Adjustment: Improving Your Financial System

The Objective:

Make smarter decisions next month

Types of Adjustments:

Expense Adjustments

- Reduce unnecessary spending

- Reallocate funds toward priorities

Behavioral Adjustments

- Avoid known triggers

- Set stricter limits

Structural Adjustments

- Modify budget percentages

- Automate savings/investments

The Power of Small Changes

Minor adjustments made consistently:

- Compound over time

- Lead to significant improvements

Insight from Authority

As James Clear states:

“Small habits don’t add up—they compound.”

The Monthly Financial Cycle

The Financial Control Loop operates on a monthly rhythm:

Week 1–4:

- Track daily spending

End of Month:

- Review all financial activity

Beginning of New Month:

- Adjust allocations and strategy

Repeat

Why Monthly Reviews Work

A monthly cycle is:

- Long enough to capture patterns

- Short enough to correct mistakes quickly

The Danger of Passive Finances

Without a control loop:

- Money leaks go unnoticed

- Spending habits worsen

- Financial goals remain unmet

The Nigerian Context: Why This System Is Essential

In Nigeria:

- Prices fluctuate rapidly

- Income may be irregular

- Social spending pressures are high

Without Control:

- Financial instability increases

- Savings are inconsistent

- Growth becomes difficult

With Control:

- Spending becomes intentional

- Priorities are enforced

- Financial resilience improves

The Psychological Advantage

The Financial Control Loop reduces:

- Decision fatigue

- Emotional spending

- Financial anxiety

It replaces them with:

- Clarity

- Structure

- Confidence

The Identity Shift

To benefit from this system, you must move from:

- “I manage money casually”

To:

“I actively control and optimize my finances.”

Practical Implementation Guide

Step 1: Choose a Tracking Method

- Spreadsheet

- App

- Notebook

Step 2: Categorize Your Expenses

- Essentials

- Lifestyle

- Growth

Step 3: Schedule Monthly Review

- Fixed date (e.g., last day of the month)

Step 4: Analyze Patterns

- Identify top spending categories

- Highlight waste

Step 5: Make Adjustments

- Refine your allocation

- Improve discipline

The Compounding Effect of the Control Loop

Over time, this system leads to:

- Better spending habits

- Increased savings

- Stronger investments

- Financial growth

The Real Transformation

When you implement the Financial Control Loop:

You move from:

- Confusion → Clarity

- Reaction → Control

- Stagnation → Progress

The Hard Truth

Most people are not financially stuck because:

- They don’t earn enough

They are stuck because:

They don’t review and improve their financial behavior.

Conclusion: Control Creates Progress

Money unmanaged:

- Drifts

- Disappears

- Disappoints

Money controlled:

- Aligns

- Grows

- Multiplies

Final Thought

At the end of this month, pause and ask yourself:

“Do I know exactly where my money went—and what I will do differently next month?”

Because until you can answer that clearly:

Your money is controlling you—not the other way around.

👉 Do you control your money—or does it control you? Find out on WealthQuizzes