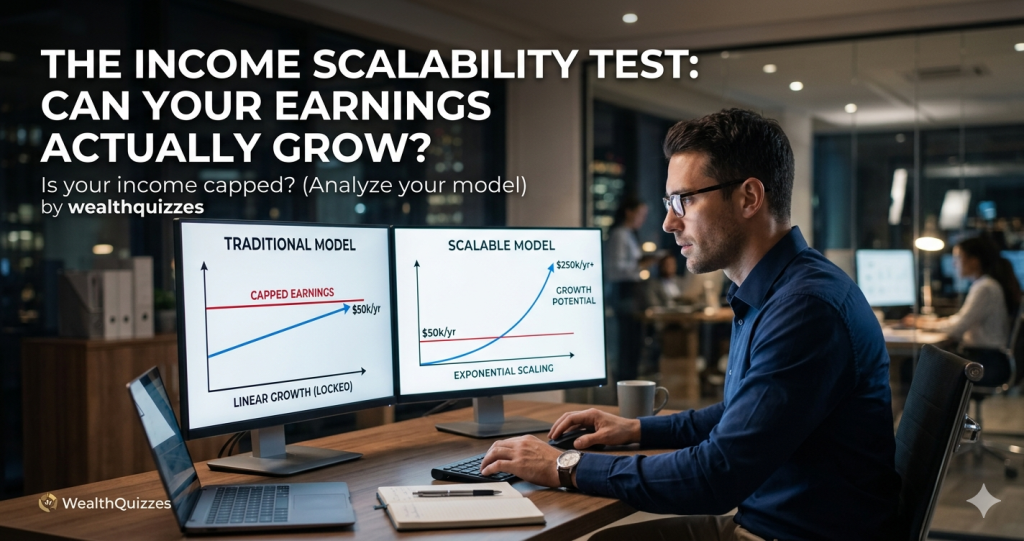

The Income Scalability Test: Can Your Earnings Actually Grow?

The Income Scalability Test: Can Your Earnings Actually Grow? Why Some Income Models Keep People Busy—but Financially Stuck Introduction: The Hidden Ceiling Most People Never Notice Many people work harder every year yet experience only limited financial progress. They: Take on more work Extend working hours Increase effort Chase additional clients Add side hustles Yet […]

The Wealth Identity Stack: Habits, Environment, and Standards

The Wealth Identity Stack: Habits, Environment, and Standards Why Wealth Is Less About Luck—and More About Behavioral Architecture Introduction: The Hidden Structure Behind Financial Success Many people believe wealth is primarily created through: High income Business opportunities Good investments Education Economic luck While these factors matter, they do not fully explain why some individuals consistently […]

The Financial Energy Principle: Where Attention Creates Wealth

The Financial Energy Principle: Where Attention Creates Wealth Why Your Focus May Be the Most Valuable Financial Asset You Have Introduction: The Hidden Link Between Attention and Wealth Most people think wealth is created primarily through: Hard work High income Business ownership Investments Education While all these matter, there is a deeper force quietly shaping […]

The Strategic Spending Model: Spending Like the Wealthy

The Strategic Spending Model: Spending Like the Wealthy Why Smart Spending Is Not About Looking Rich—But Building Financial Leverage Introduction: The Hidden Difference Between Rich-Looking and Wealthy Many people assume wealthy individuals simply: Spend more Buy luxury items Live extravagantly Upgrade constantly But genuine wealth creation often operates very differently from popular perception. One of […]

The Wealth Protection Blueprint: Keeping What You Build

The Wealth Protection Blueprint: Keeping What You Build Why Building Wealth Is Only Half the Battle—and Protecting It Is the Other Half Introduction: The Wealth Most People Lose Too Easily Many people spend years trying to: Earn more money Build businesses Acquire assets Increase investments Improve financial stability Yet surprisingly, many financially successful individuals still […]

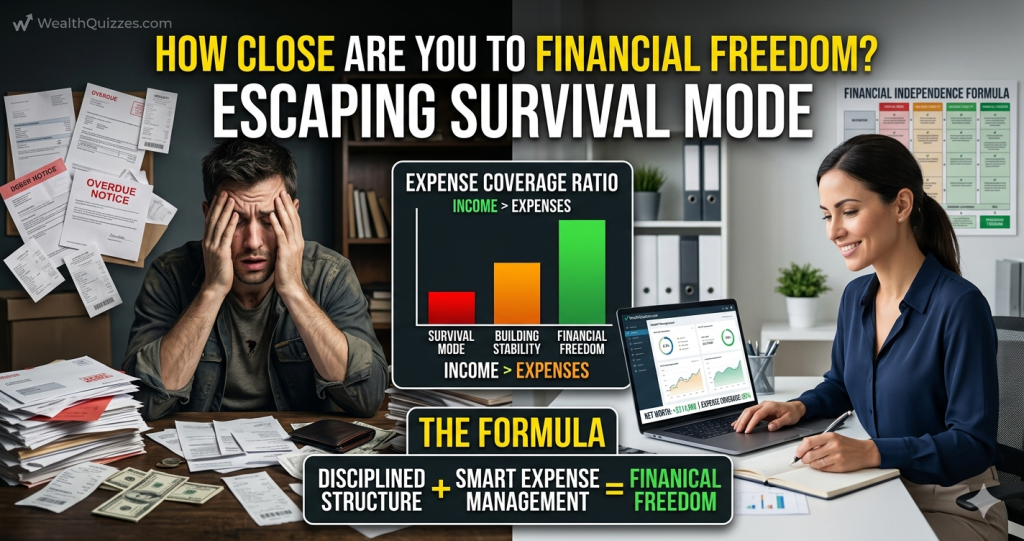

The Financial Independence Formula: Escaping Survival Mode

The Financial Independence Formula: Escaping Survival Mode Why Financial Freedom Is Less About Luxury—and More About Structure Introduction: The Trap of Permanent Survival Mode Millions of people work hard every day yet remain trapped in a financial cycle that feels impossible to escape. The pattern is familiar: Earn money Pay bills Solve urgent problems Start […]

The Cash Flow Engine: Building Money-Producing Systems

The Cash Flow Engine: Building Money-Producing Systems Why Financial Stability Depends on Repeatable Income, Not Occasional Earnings Introduction: The Problem With Unpredictable Money Many people work extremely hard yet remain financially unstable because their income system depends entirely on: Constant effort Daily labor One-time transactions Unpredictable opportunities The result is a frustrating cycle: Earn money […]

The Invisible Wealth Killers: Inflation, Taxes, and Lifestyle Drift

The Invisible Wealth Killers: Inflation, Taxes, and Lifestyle Drift How Silent Financial Forces Slowly Destroy Wealth Without Most People Realizing It Introduction: The Financial Threats Most People Never Notice When people think about losing money, they often imagine: Business failure Job loss Bad investments Economic crises But in reality, some of the greatest threats to […]

The Capital Allocation Mindset: Why Wealthy People Think in Percentages

The Capital Allocation Mindset: Why Wealthy People Think in Percentages How Financial Destiny Is Determined Less by Income—and More by Allocation Introduction: The Hidden Difference Between the Rich and Everyone Else Most people focus heavily on: How much money they earn Wealthy people focus heavily on: Where money goes This distinction appears simple, but it […]

The Wealth Flywheel: How to Build Self-Sustaining Financial Growth

The Wealth Flywheel: How to Build Self-Sustaining Financial Growth Why True Wealth Is Built Through Momentum, Not Constant Struggle Introduction: The Problem With Starting Over Financially Many people experience the same frustrating cycle repeatedly: Earn money Make progress Encounter expenses Lose momentum Start over again This financial “reset loop” prevents long-term wealth accumulation. Even hardworking […]